Click to share on Facebook

This article first appeared on Renew Economy on 19 October 2015

There’s an old saying that what counts is what gets counted, there’s a less well-known adage that says, what doesn’t get counted can cost you a fortune. The Australian insurance industry is finding out all about that one now because over the last five years the industry has dropped the ball when it comes to managing the risk posed by climate change.

There are three reasons why they have failed shareholders and customers; a lack of sufficient research, reporting and an almost complete absence of collaboration nationally or internationally. And these three failures stem from a lack of leadership within the industry itself.

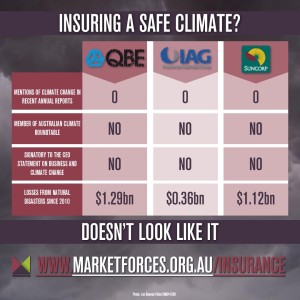

Since 2010 each of the major general insurers have incurred significant losses where claims exceeded natural disaster provisions: IAG $364million, QBE $1.29billion and Suncorp $1.12billion.

That natural disasters are on the increase should not come as a surprise to anyone, particularly insurers. As Andrew Pitman, director of the ARC Centre of Excellence for Climate System Science at the University of New South Wales, told Fairfax Media recently “without any doubt whatsoever” the trend of insured losses linked with natural disasters were on the rise and would continue to soar and this could also lead to reducing coverage in some areas.

The first reason why the industry is getting it so wrong when it comes to pricing and managing natural disaster provisions is because it is not doing its homework particularly when it comes to research and reporting. It has been missing in action since 2008, when IAG was a leading industry figure on climate change under the tenure and thought leadership of CEO Michael Hawker and CRO Tony Coleman.

Consider this: of the three major general insurers, none have published or spoken substantively on climate change and its effects on the industry since 2010 (IAG); QBE and Suncorp have not published any research or spoken on the issue at all.

The peak industry body, The Insurance Council of Australia, has published just one report regarding climate change and it merely deals with adaptation and resilience. The Insurance Council has made just three submissions to all levels of government concerning climate change in its history and those related to adaptation and natural disaster funding arrangements.

The insurance regulator, APRA, has not published a single report on climate change nor on its potential impacts on the insurance industry or the broader financial system. Sure the industry sponsors research groups like, Risk Frontiers, but most of its publications are not for public consumption, nor is it ever re-published by any of the major insurers.

This dearth of research becomes more concerning when we remember that general insurers manage in excess of AU$80 billion; and that investment portfolios are likely to have exposure to the debt and equity of fossil fuel companies, and increasingly the infrastructure of the fossil fuel industry. Indeed the general insurers continue to underwrite the operations of fossil fuel companies.

Ironically all three major general insurers participate in the Carbon Disclosure Project (CDP), but none disclose Scope 3 emissions (which would include the businesses they underwrite and their investment portfolios).

As the rest of the finance sector struggles to come to grips with a carbon-constrained world, the insurance industry is a notable absence in a number of leading forums like the Australian Climate Roundtable – none of the major insurers or the Insurance Council has joined. Likewise no major insurer was a signatory to the recent CEO Statement on Business and Climate Change and the Paris Negotiations. And only IAG is a member of The Geneva Association that encourages investment in low-carbon energy projects, but there is no indication IAG have made such investments.

Compare this level of engagement – or disengagement – with its UK and EU counterparts. The Bank of England Prudential Regulatory Authority recently published a report entitled “The impact of climate change on the UK insurance sector”. The report was subsequently endorsed by fifteen CEOs of various UK insurance companies and they demanded urgent action on climate change. While in Europe Allianz, AXA, Munich Re and Swiss Re report widely on the issue and have committed to strong climate action and are changing their businesses accordingly.

Defenders of the insurance industry could argue the political climate in Australia under Tony Abbott had made any meaningful discussion about climate change and its impacts extraordinarily difficult. Nevertheless shareholders and customers are about to wear the financial cost of this lack of leadership.

More than most industries the insurance industry is on the frontline of climate change. Their profitability will continue to be impacted by natural disasters. Endlessly increasing premiums until customers are priced out, or not offering coverage at all are not long-term solutions. Regardless of national political pressure customers and shareholders rightly expect the industry to be consistently outspoken advocates for tough action on climate change, which includes lobbying government, publishing research on climate change impacts, speaking publicly in favour of carbon pricing and working in collaboration with other sectors of business and finance.

Certainly the first sign of insurance companies taking climate change seriously would be to stop underwriting fossil fuel projects, stop investing in fossil fuel companies and start investing in renewable energy.

Find out more about Australia’s insurance companies and their approach to climate change here.