Report

Investor Disconnect on Climate Risk

Executives reveal mismatch between reality of climate risks and corporate reputation

It is widely recognised that the world must swiftly cut fossil fuel use if it is to avert catastrophic climate change. Institutional investors play a crucial role in this transition due to their vast financial leverage and as the principal owners of some of the world’s biggest fossil fuel companies. Climate risks also have significant potential impacts on investments and portfolios, and the stability of economies. Recognising this, many big-name institutional investors have signed up to initiatives like Climate Action 100+, the Net Zero Asset Managers initiative (NZAM), Net Zero Asset Owner Alliance (NZAOA) and Principles for Responsible Investment (PRI).

However, the extent to which the frameworks developed by these groups are genuinely integrated into real-world investment processes remains unclear, with institutional investors frequently engaging in actions that appear to contradict them. Previous research1 has found that while investors recognise the importance of climate risks, integrating them at a practical level across the industry is still in its infancy. Market Forces sought to build on this research to better understand how climate risk considerations are currently being applied by institutional investors in practice, and the key barriers to further integration.

In September to November 2023, Market Forces conducted an online survey of 150 investors at some of the world’s biggest financial institutions across the UK, USA, Singapore, Japan, Australia, Hong Kong and Belgium, delivered in partnership with NewtonX. Participants were senior decision makers within their company, working at ‘c-suite’ level – chief executive officer (CEO), chief investment officer (CIO), etc. – through to investment analyst/strategist level (see Methodology for details). This report outlines the key findings from the research.

This is an important topic which seemed to be losing traction and media attention. The inflationary environment coupled with cost pressures have contributed to waning interest and discouraging investors, governments and public to tackle this important topic as a priority it deserves.

Summary of key findings

1. Investors are more concerned about reputational risk to their company than the social and environmental impacts of the companies they invest in – Respondents indicated that reputational risk to their company and client returns influenced their investment decision making the most, while environmental performance and climate change impacts of investee companies were amongst the least influential considerations.

2. Investors are overlooking scope 3 emissions as a key indicator of regulatory and reputational risk – A large proportion of respondents indicated they largely disregard scope 3 emissions when evaluating investments and respondents were overall far more concerned about government regulation and reputational risk. Scope 3 emissions – those that a company is indirectly responsible for up and down its value chain – are a key indicator of material regulatory and reputational risks, especially for upstream fossil fuel companies. By overlooking scope 3 emissions, investors are failing to fully consider exposure to risks they are most concerned about.

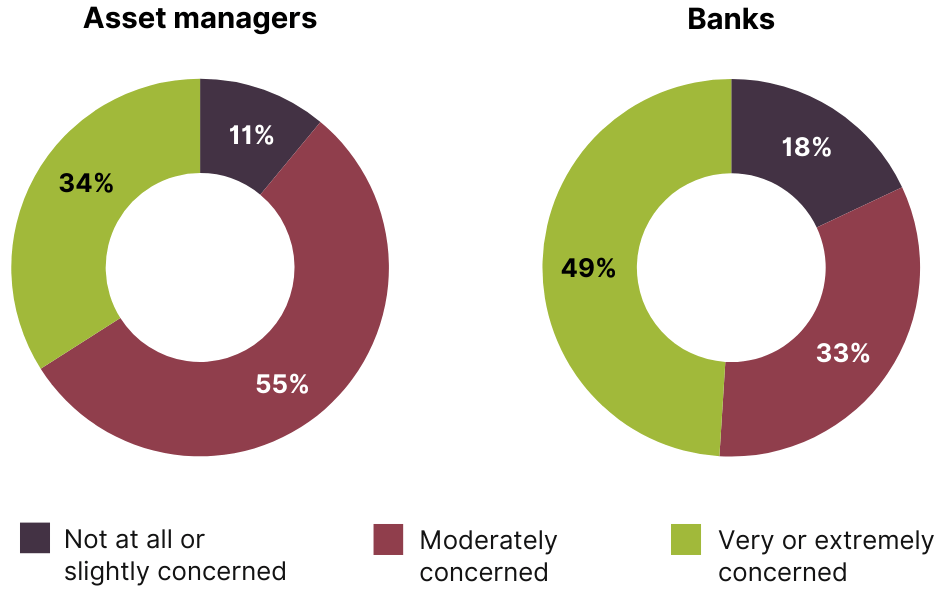

3. The overwhelming majority of investors are personally concerned about climate change – 84% of respondents were moderately to extremely concerned, although significantly less so amongst US respondents.

4. Investors’ personal views on climate change appear to influence their investment decision making – Respondents with the lowest levels of personal concern about climate change were also the least likely to incorporate climate risk factors, beyond government regulation, in their evaluation of investments. This suggests some investors are allowing personal bias to dictate their investment decisions by ignoring what is objectively a profound risk to their investments.

5. Investors are overwhelmingly relying on internal modelling/analysis and investee disclosures when assessing climate risk. By contrast, the International Energy Agency (IEA) and Intergovernmental Panel on Climate Change (IPCC) scenarios modelling and analysis are disregarded by most investors.

6. Of those relying on IEA scenarios, investors’ base case forecasts were most likely to reflect the Sustainable Development Scenario. This is consistent with a rapid energy transition that limits the global temperature rise to 1.65°C by 2100 at a 50% probability.

7. Greenwashing and inadequate information from companies on their climate management plans are the main barriers to investors incorporating climate risk more effectively.

8. Investors are equally as willing to use engagement and divestment as tools for responding to climate risks. About equal proportions of respondents would opt to engage with the investee and to reduce their investment if an investee was found to be facing a high level of climate risk.

Key findings

1. Investors are more concerned about reputational risk to their company than the social and environmental impacts of the companies they invest in.

Climate risks are largely irrelevant in the HF [hedge fund] investing process save for the opportunities and risks created by the legal, regulatory and political environment around these policies. Fund managers are less concerned about climate risks than they are political/activist pressure. This is almost entirely because climate risks have very little impact on asset performance.

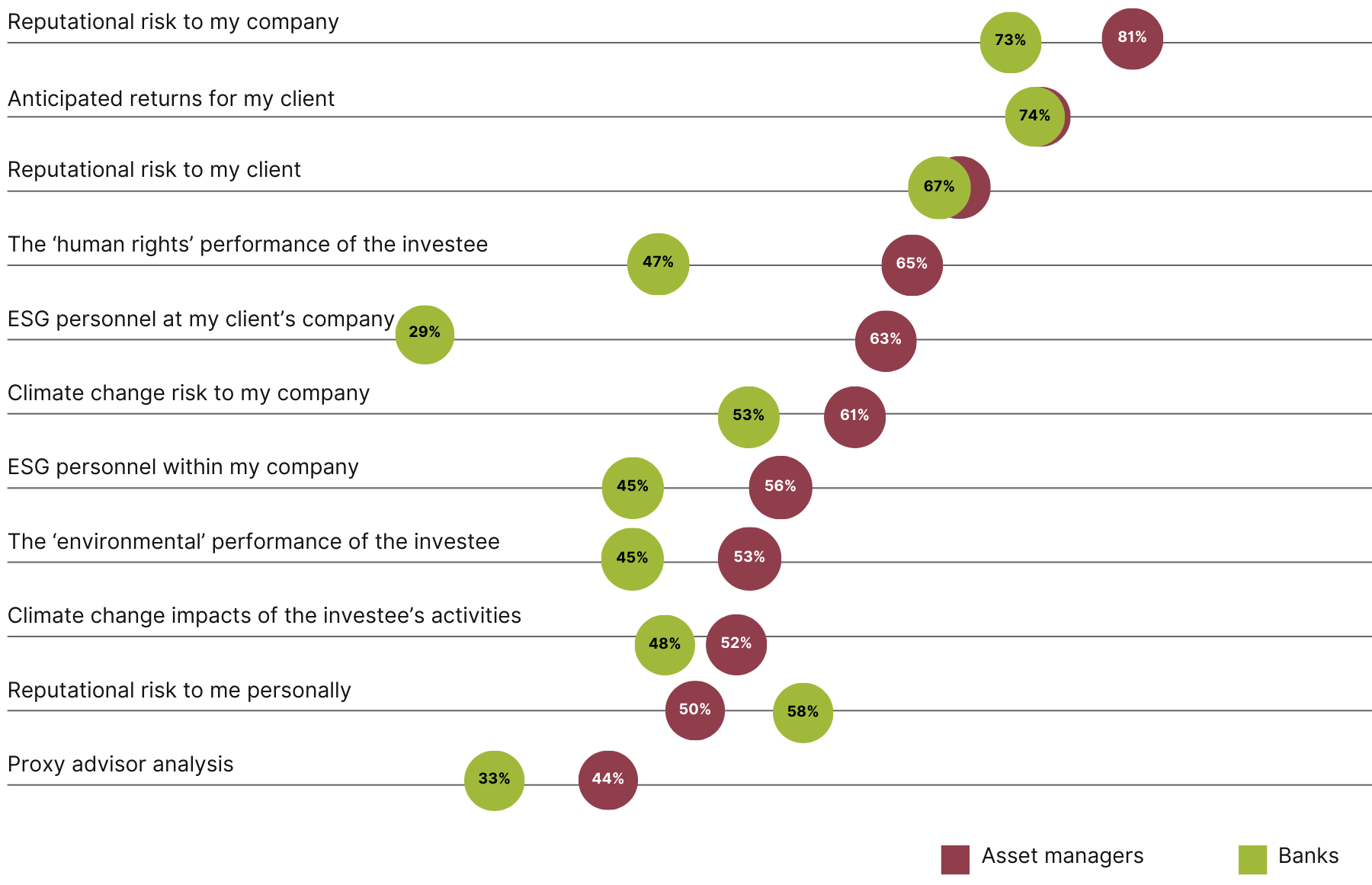

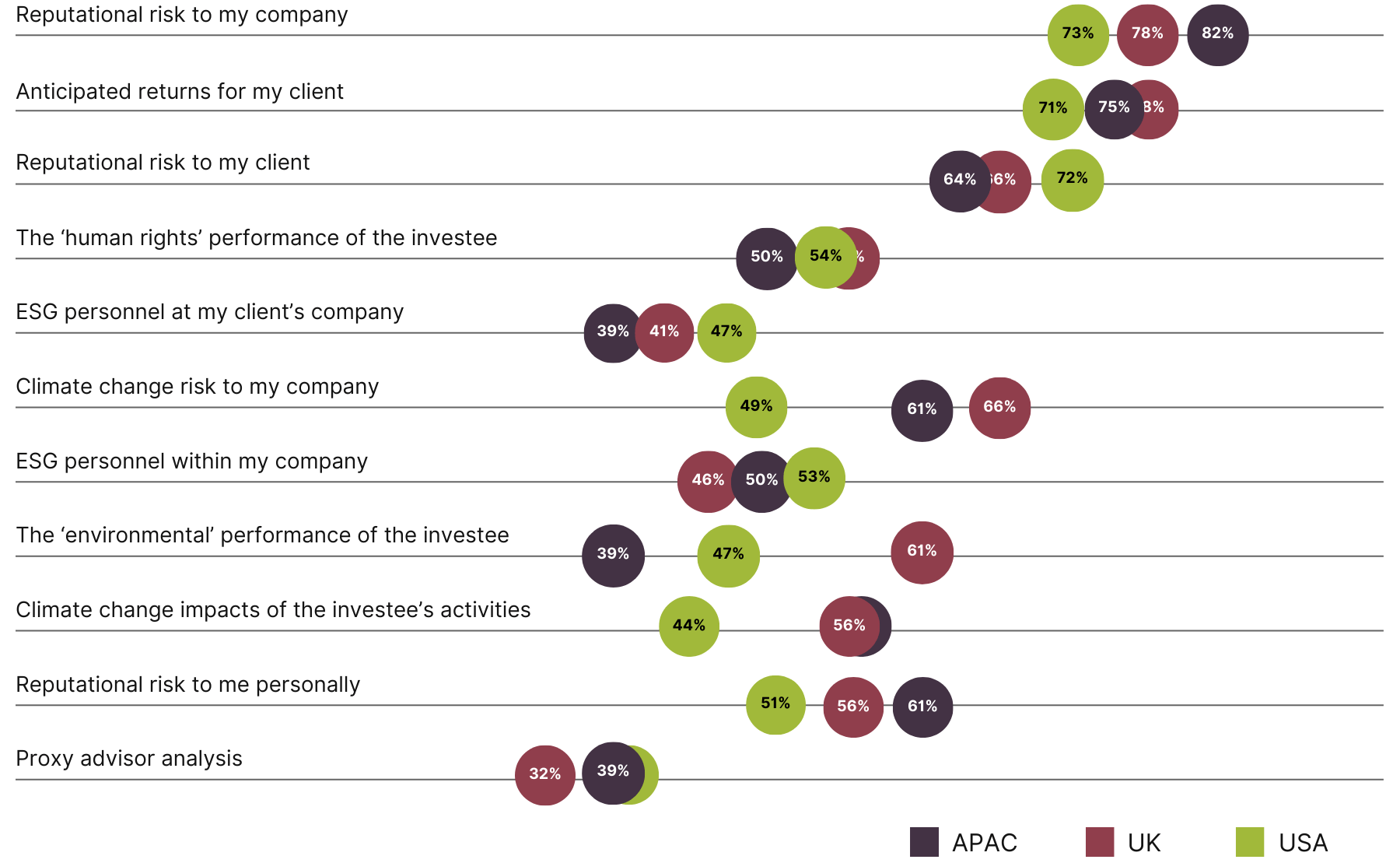

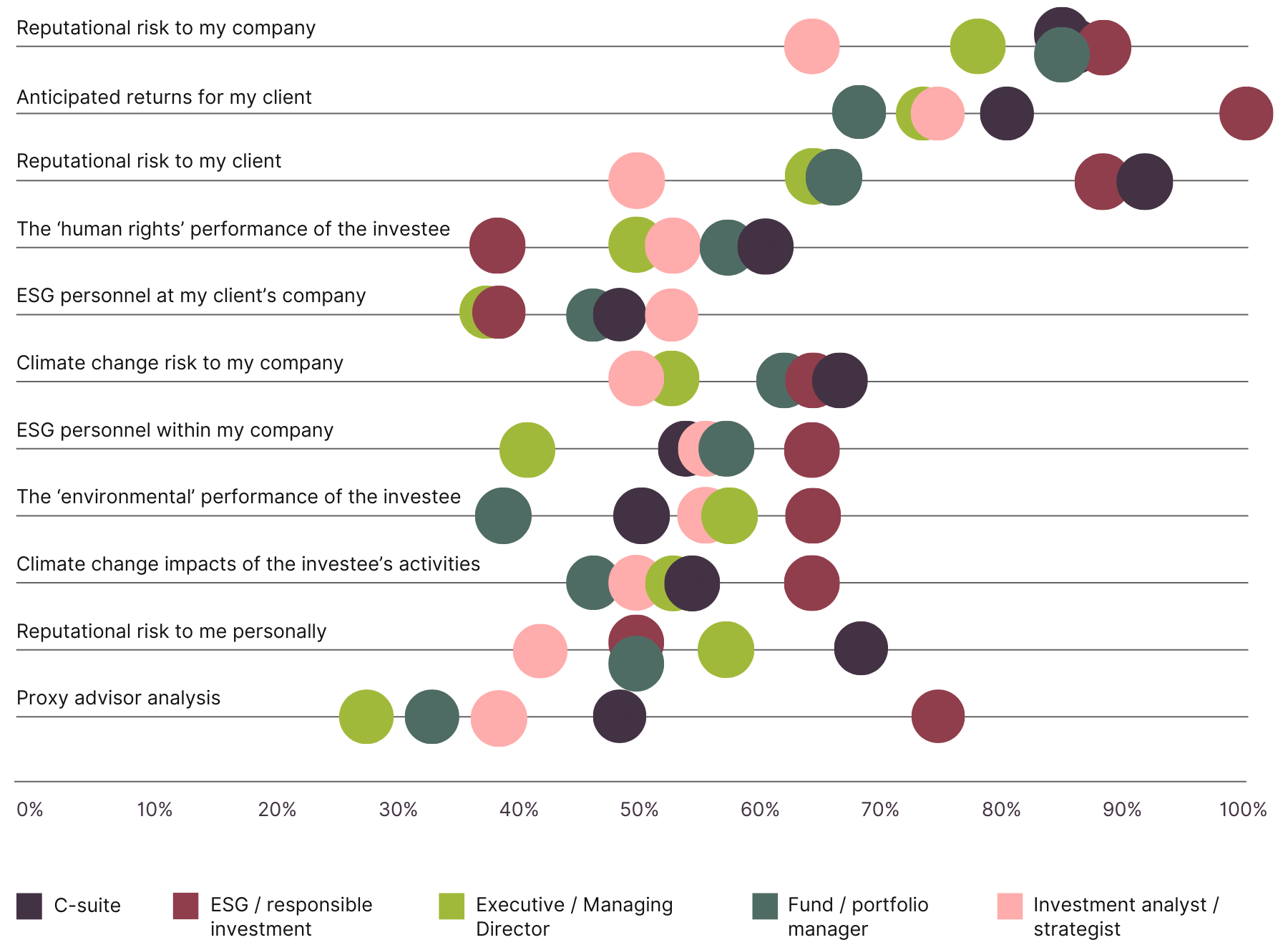

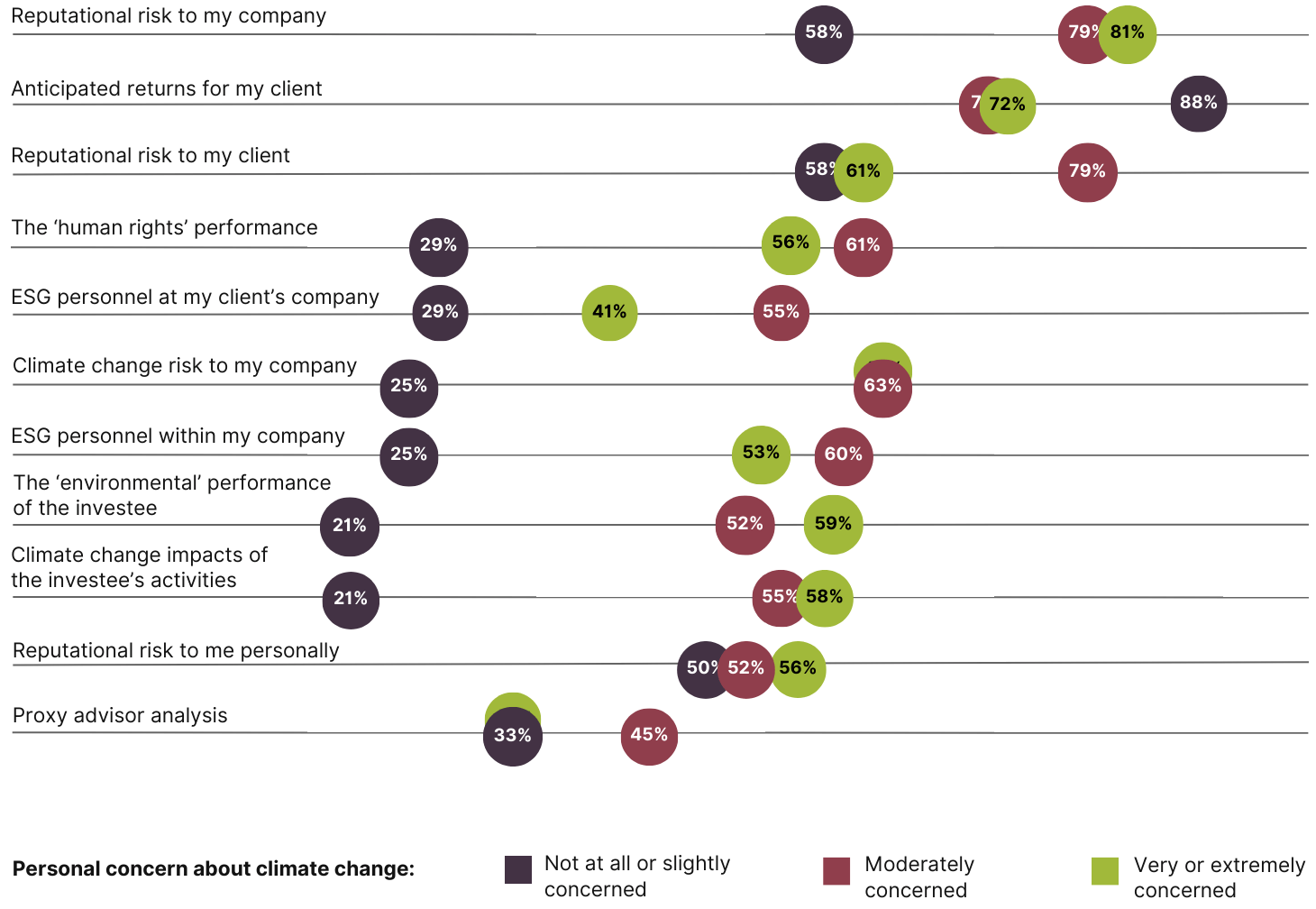

Figure 1: Influences on investor decision making when evaluating investments

Biggest challenge is tying work to financial performance. Shareholders number one priority is returns.

Figure 2: Factors with a ‘high’ or ‘very high’ level of influence on investor decision making

By company type

By region

By job role

Note: Results for ESG / responsible investment should be treated with caution due to a small sample size.

By climate concern

Any organisation that adds ESG to audit and consulting touch points is considered valuable as they can take a holistic approach

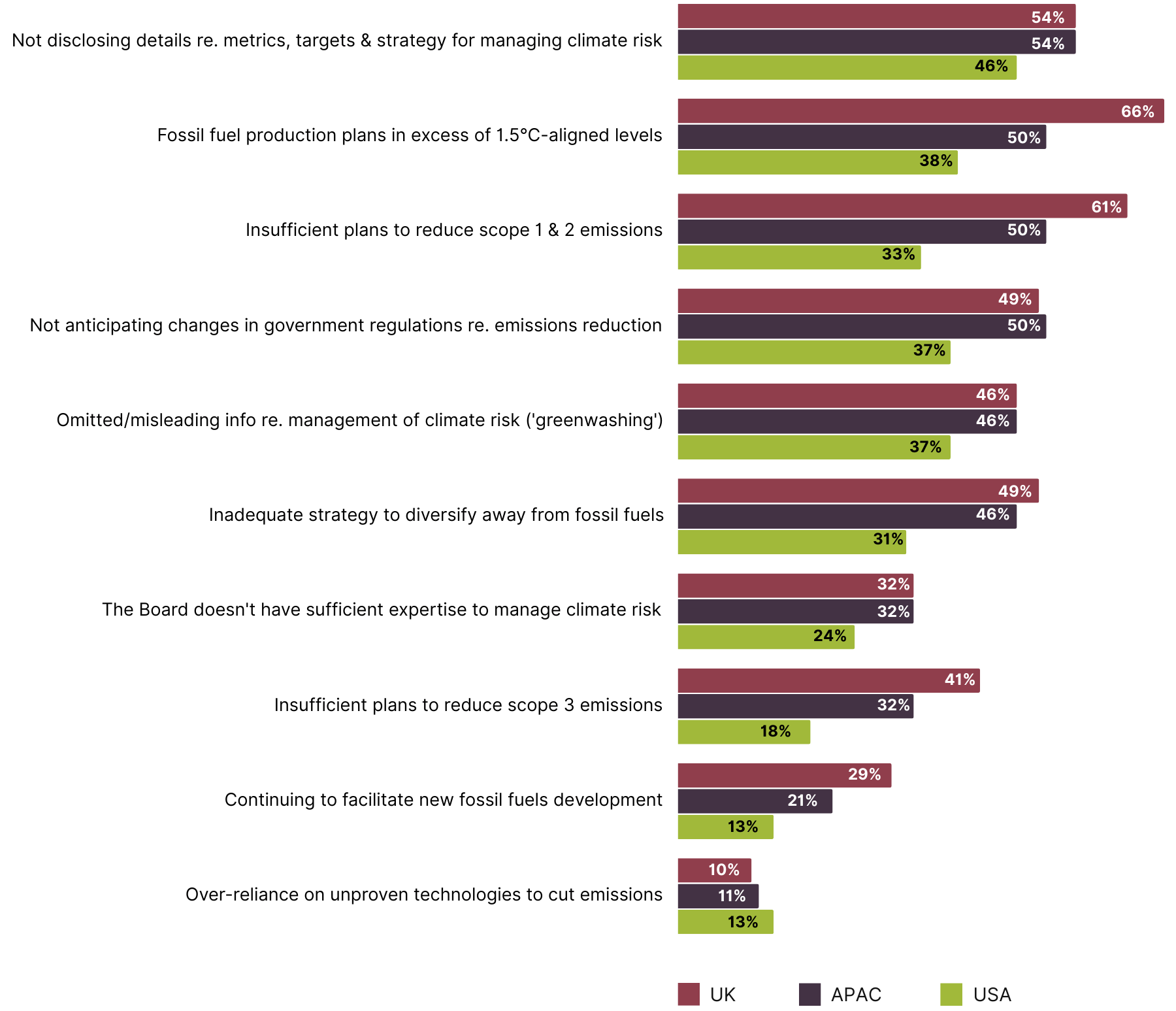

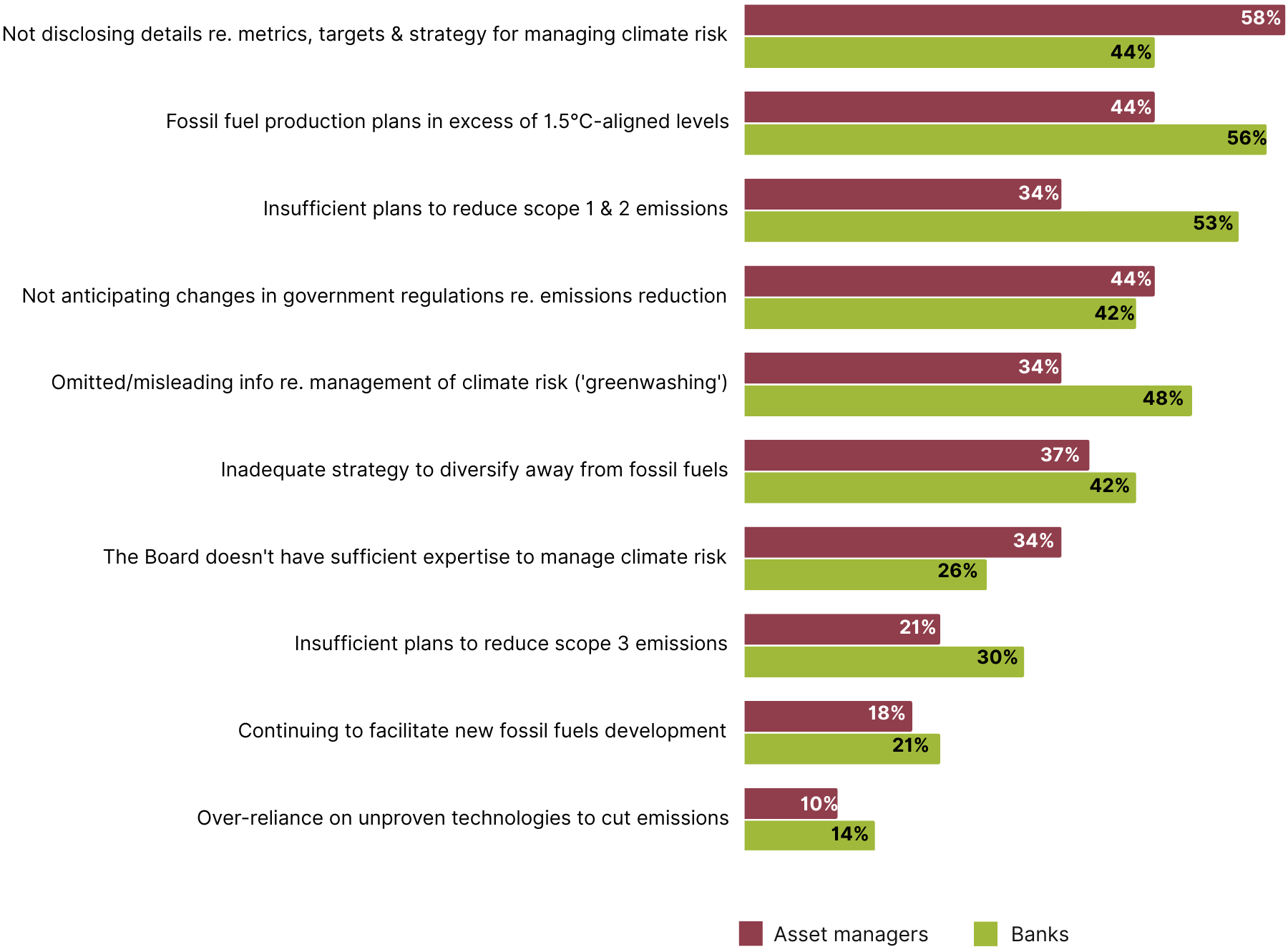

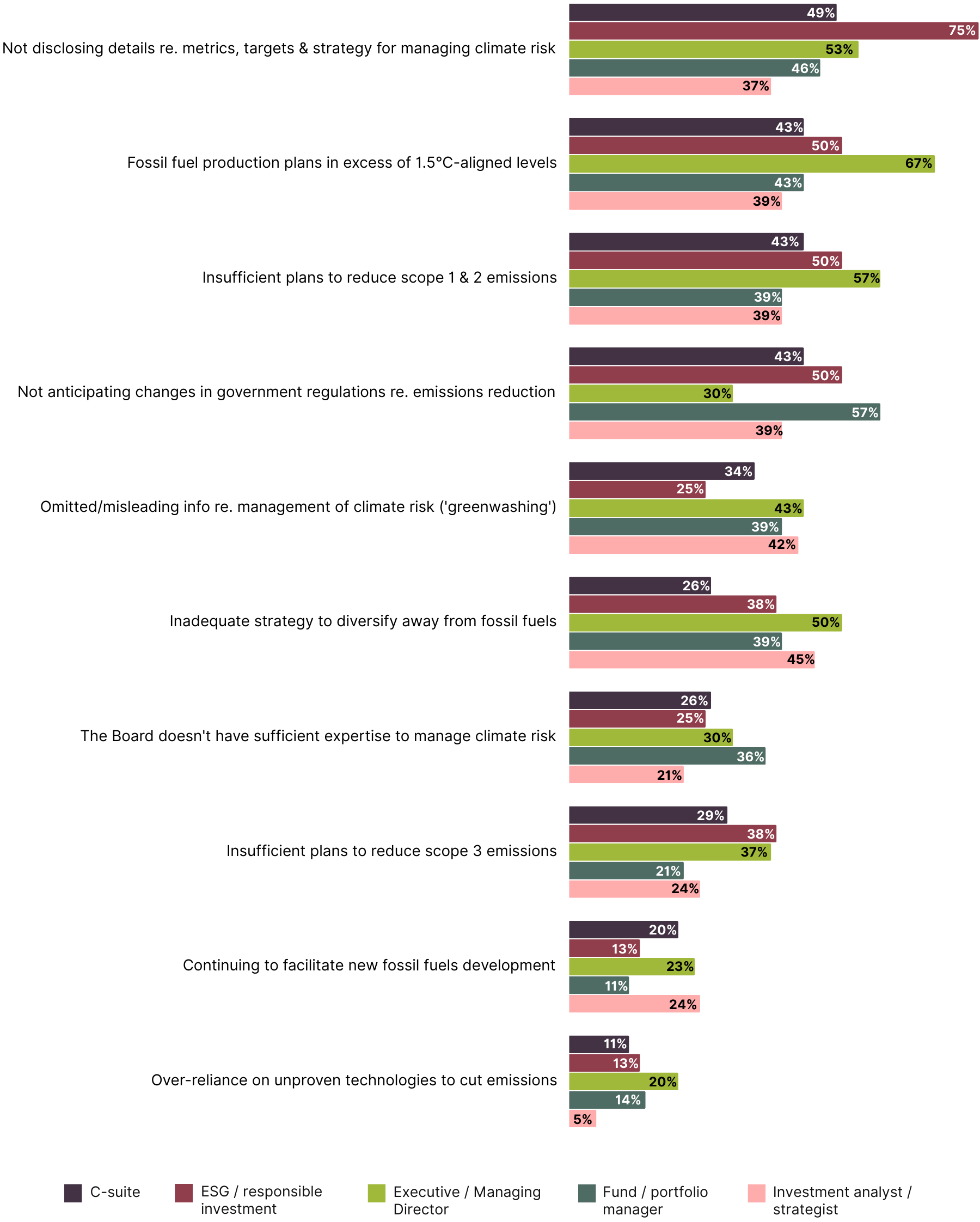

2. Investors are overlooking scope 3 emissions as a key indicator of regulatory and reputational risk

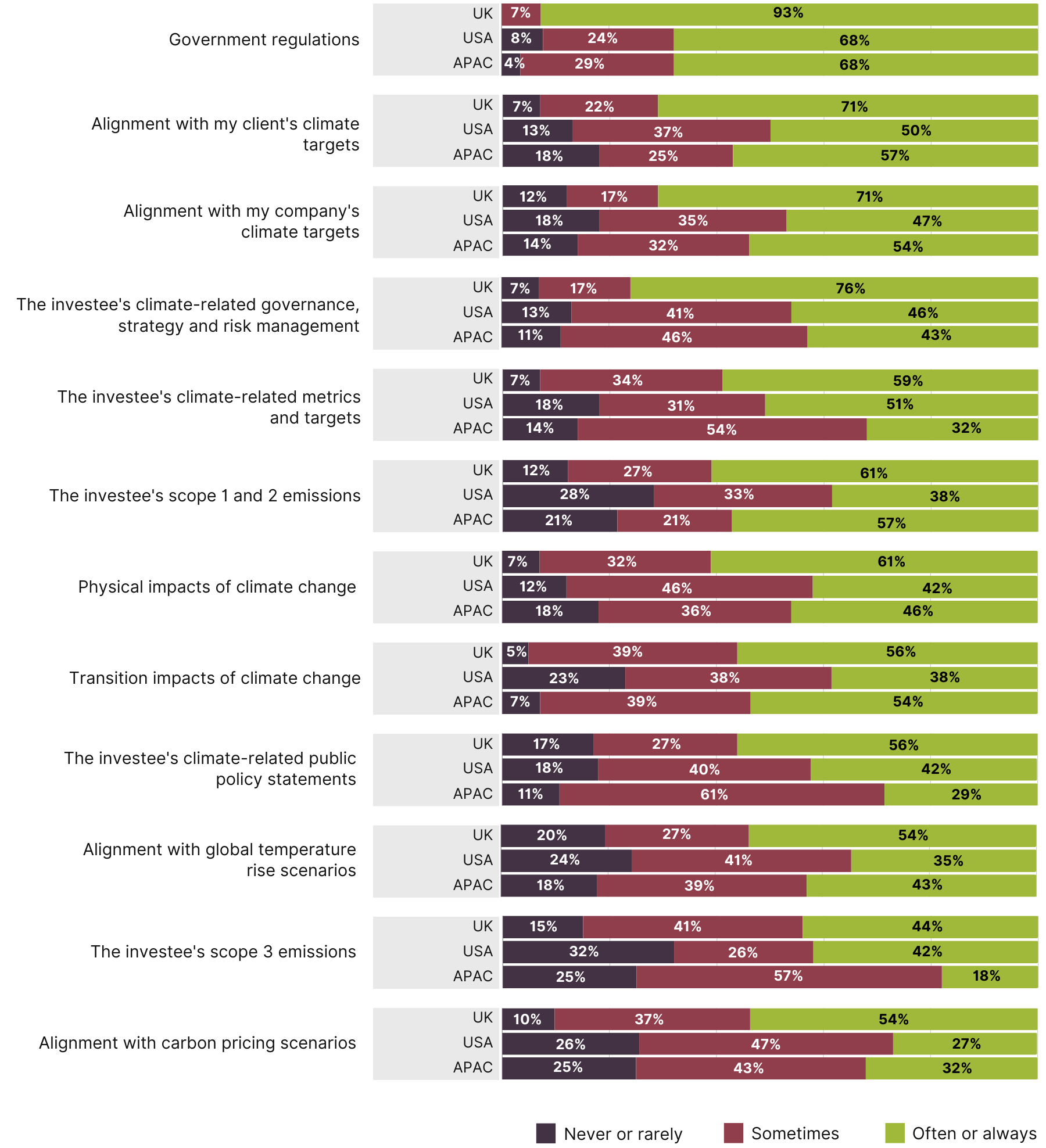

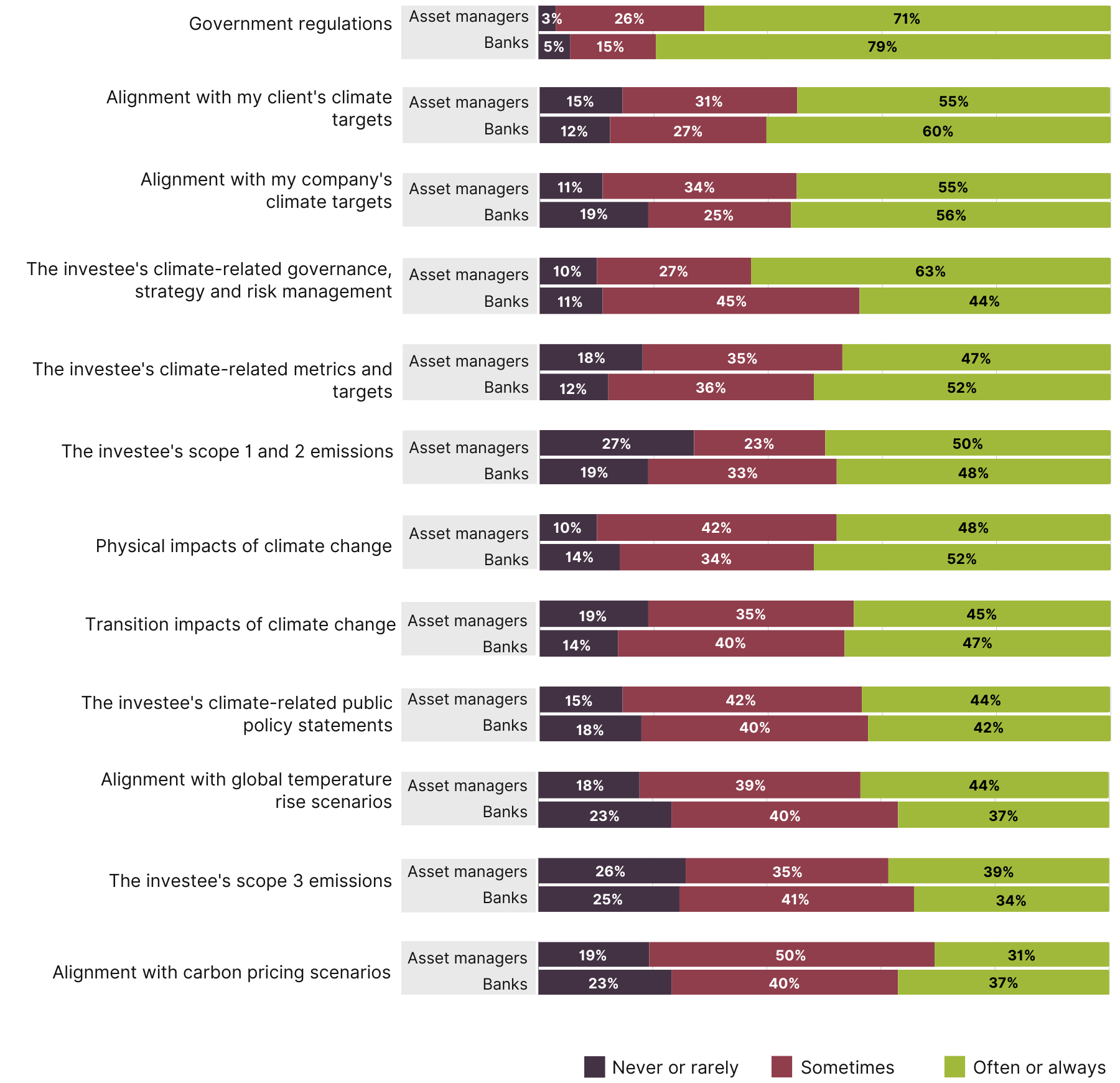

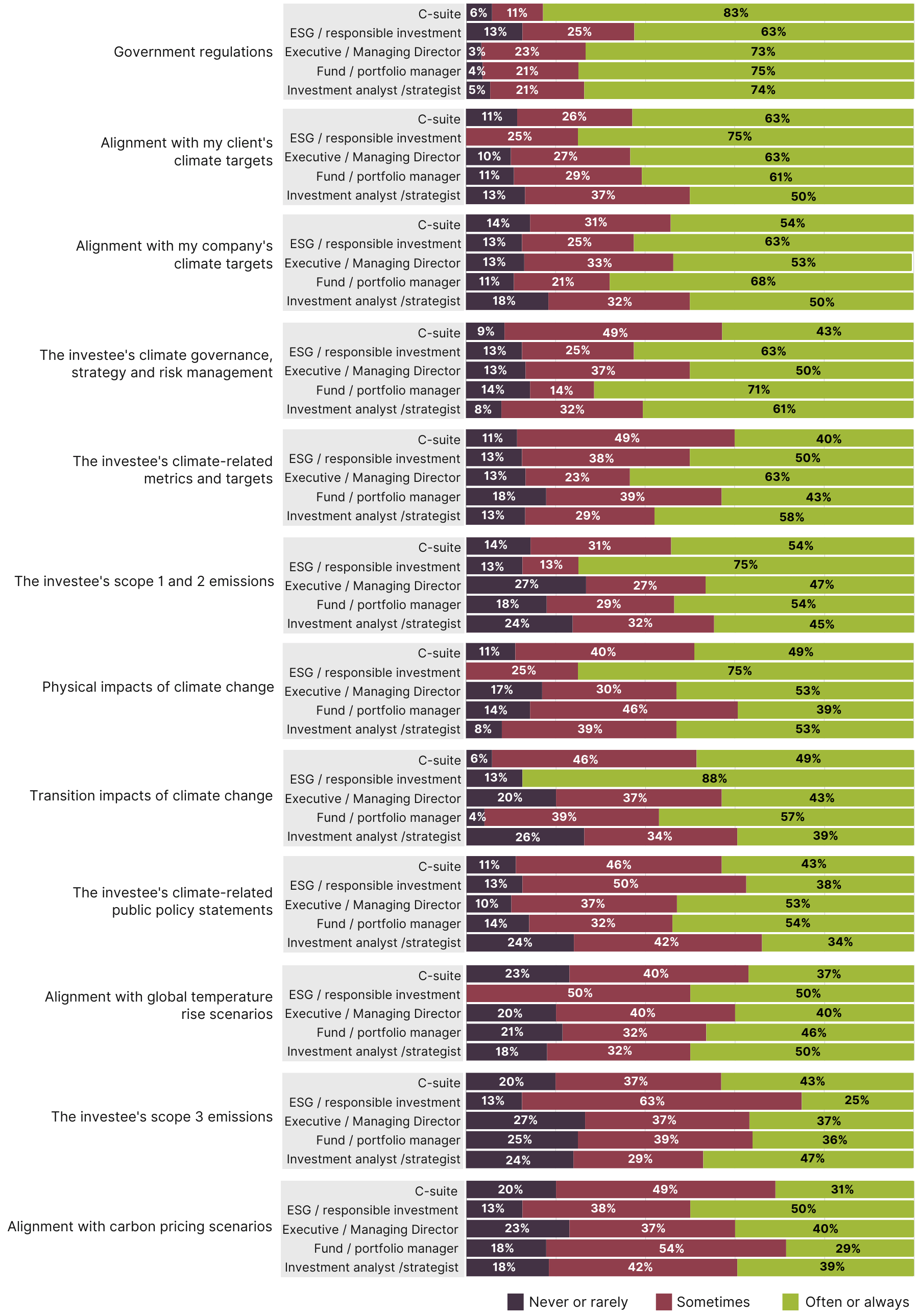

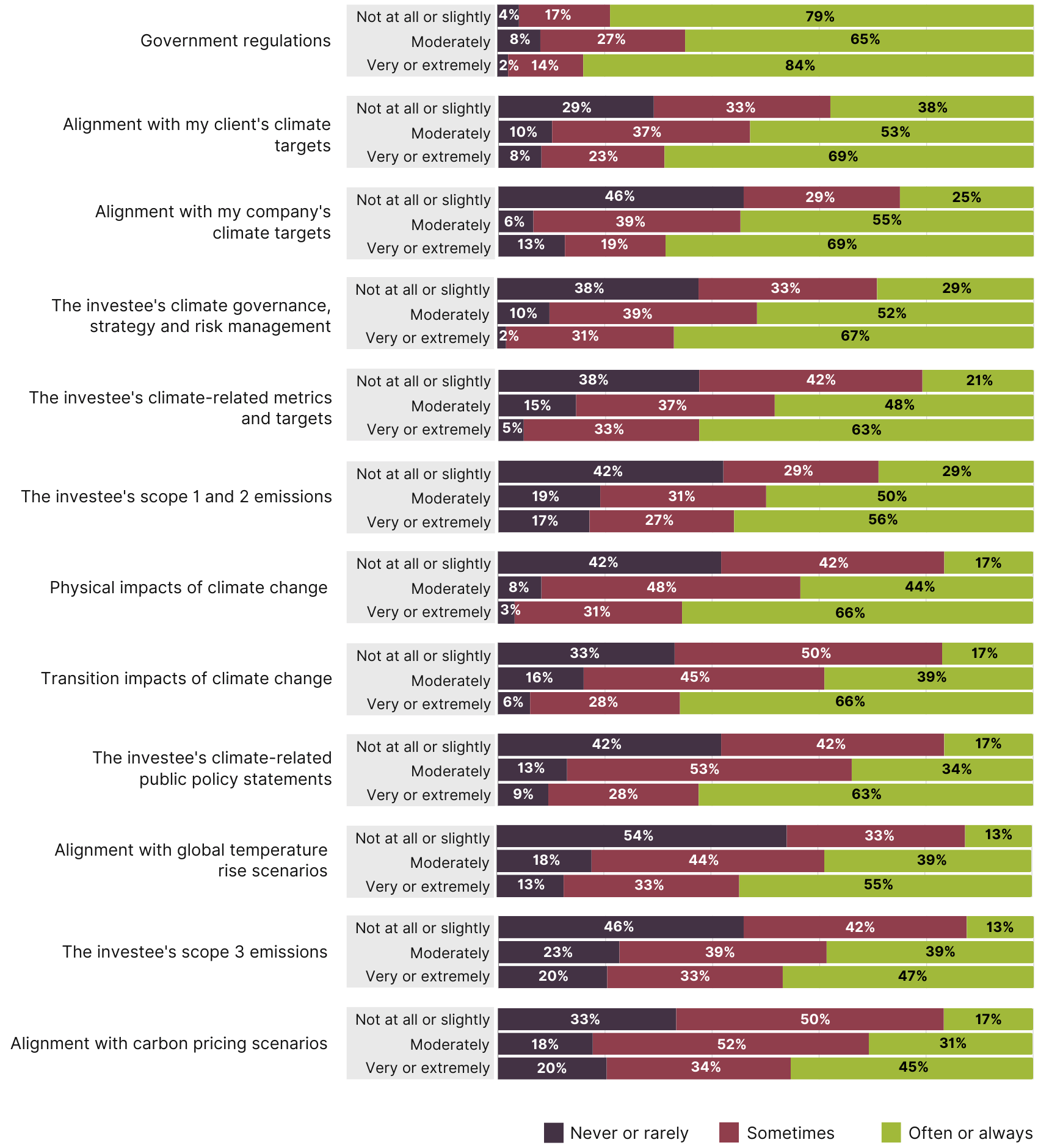

Figure 3: Climate risks considered by investors when evaluating an investment

By region

By company type

By job role

By climate concern

Figure 4: Factors that investors consider ‘high climate risk’ in an investment they are evaluating

By region

By company type

By job role

Note: Results for ESG / responsible investment should be treated with caution due to a small sample size.

By climate concern

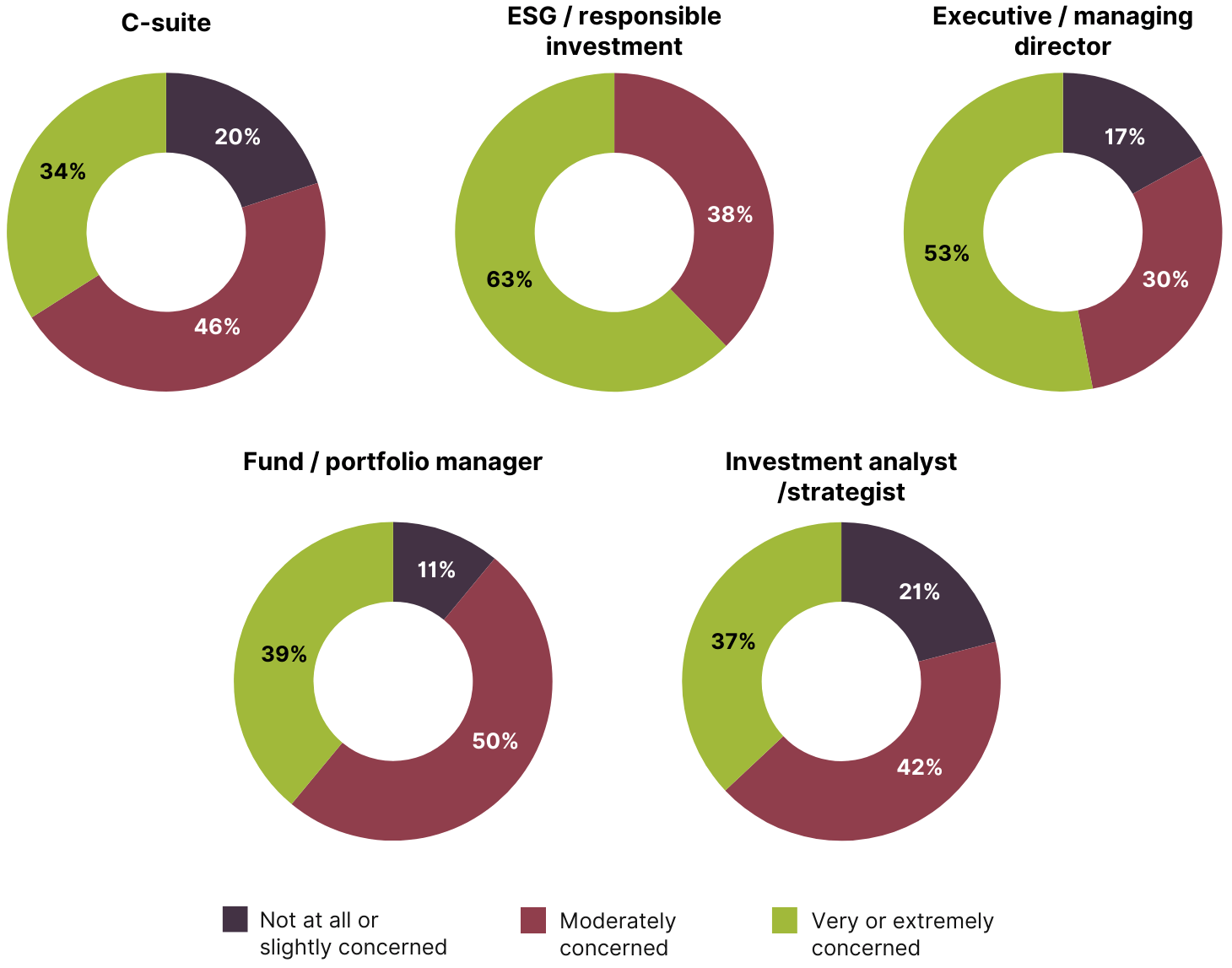

3. The overwhelming majority of investors are personally concerned about climate change.

Figure 5: Investors’ personal concern about climate change

Figure 6: Investors’ personal concern about climate change – by region

Figure 7: Investors’ personal concern about climate change – by company type

By company type

By job role

Note: Results for ESG / responsible investment should be treated with caution due to a small sample size.

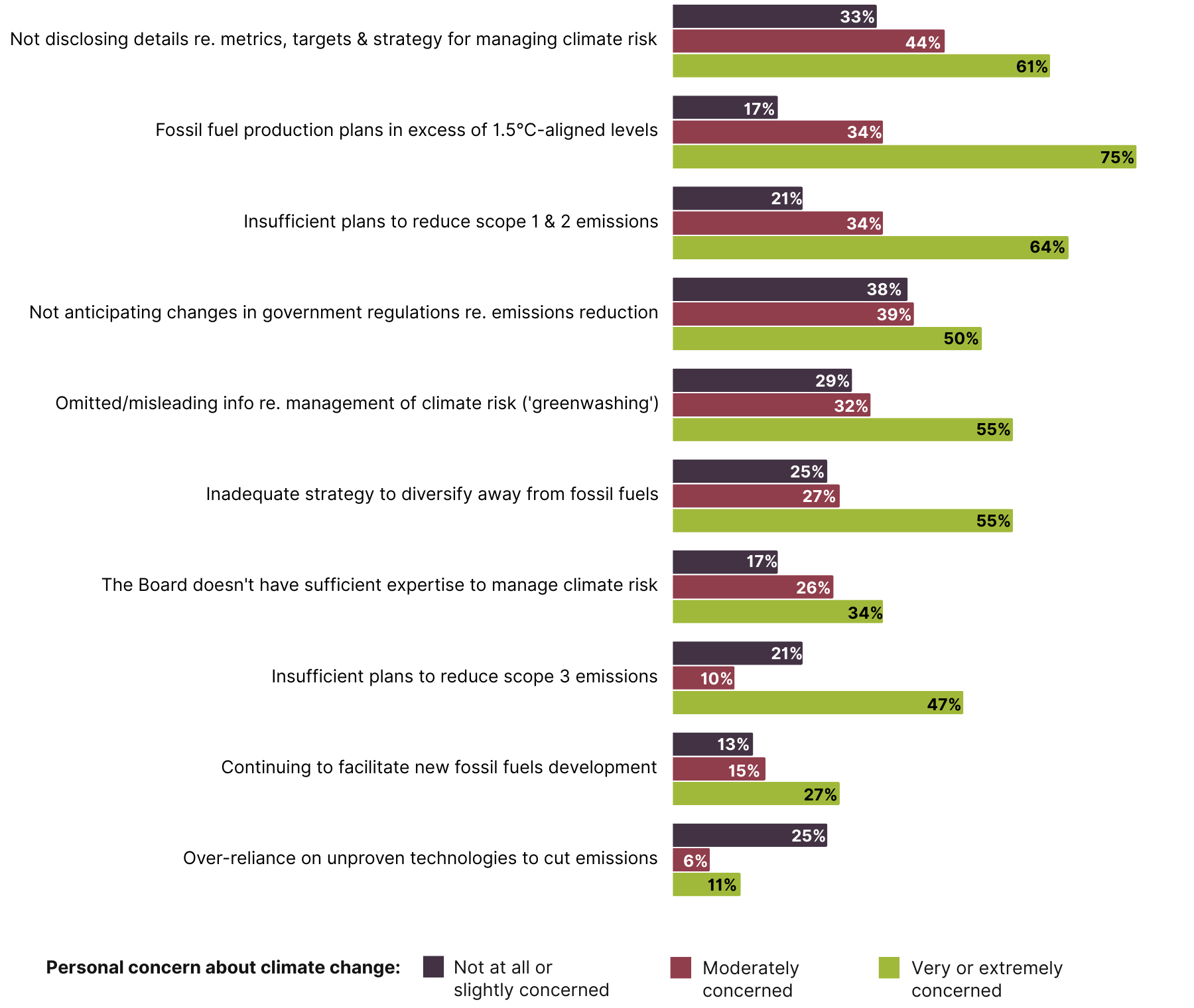

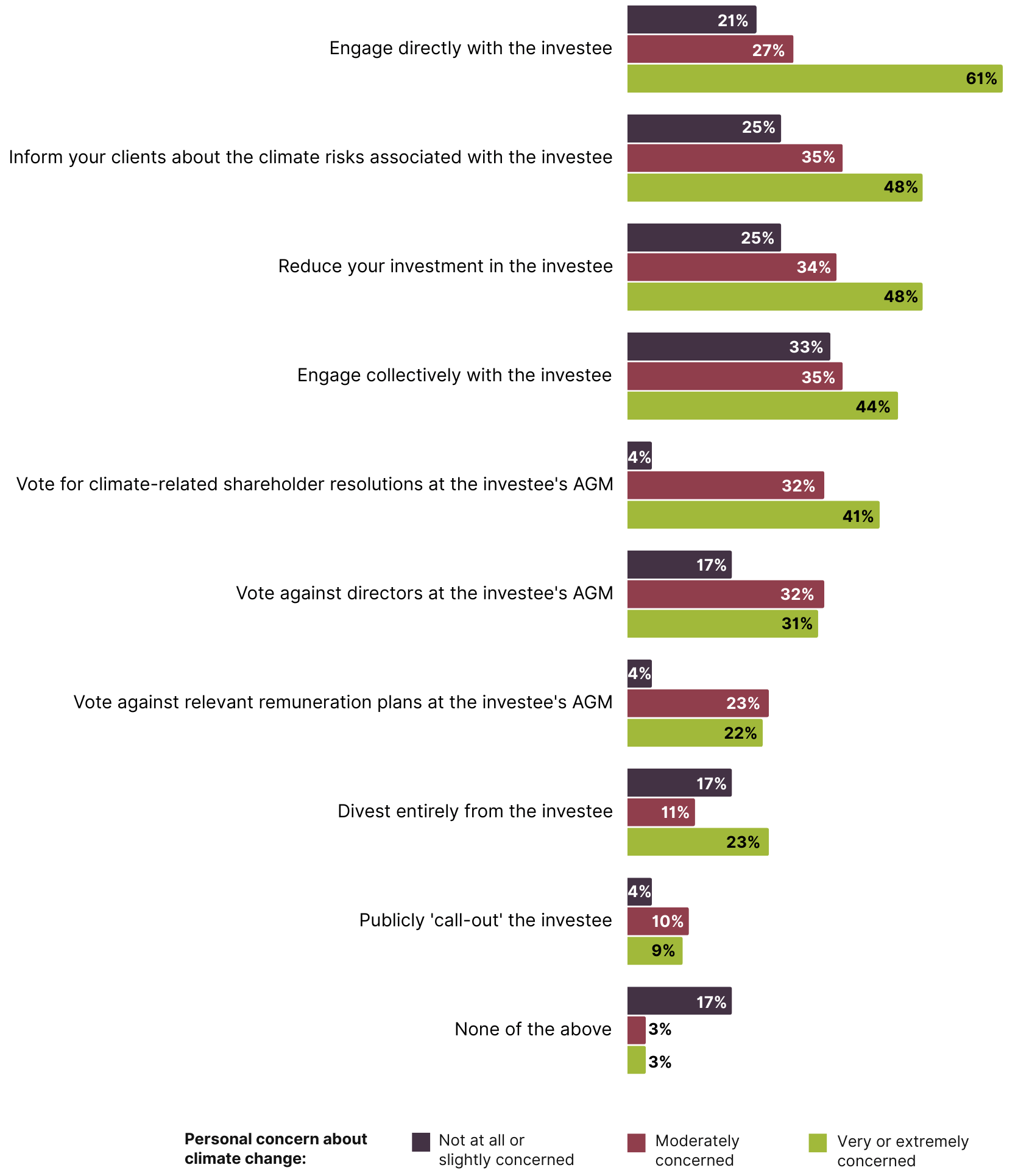

4. Investors’ personal views on climate change appear to influence their investment decision making.

Figure 8: Influence of climate risk on investor decision making – by extent of personal concern about climate change

‘Government regulation’ is a notable deviation from this trend, with even the least climate-concerned investors still clearly worried about the risk this poses to their investments.

Figure 9: Climate risks ‘often’ or ‘always’ considered by investors when evaluating an investment – by extent of personal concern about climate change

Whether an individual believes in it or not, climate change has an effect on the economy on a global scale. The amount of capital being funnelled into organizations that integrate solar, wind, and other alternative forms of energy is growing on a year-to-year basis. Not only are massive asset managers growing their ESG investing capabilities, but they are also being conscious of their own carbon footprints and taking measures that align with a greener future internally.

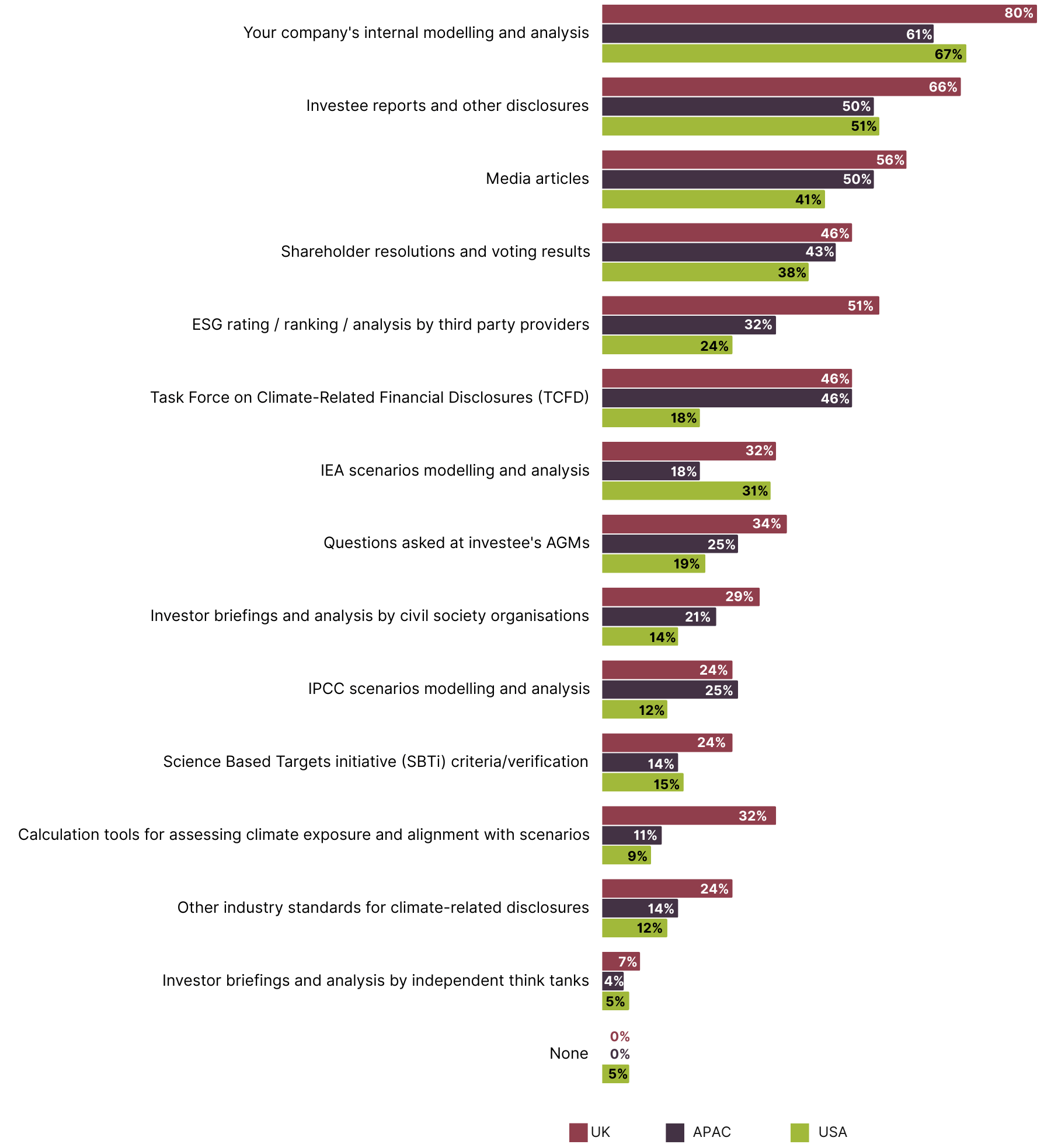

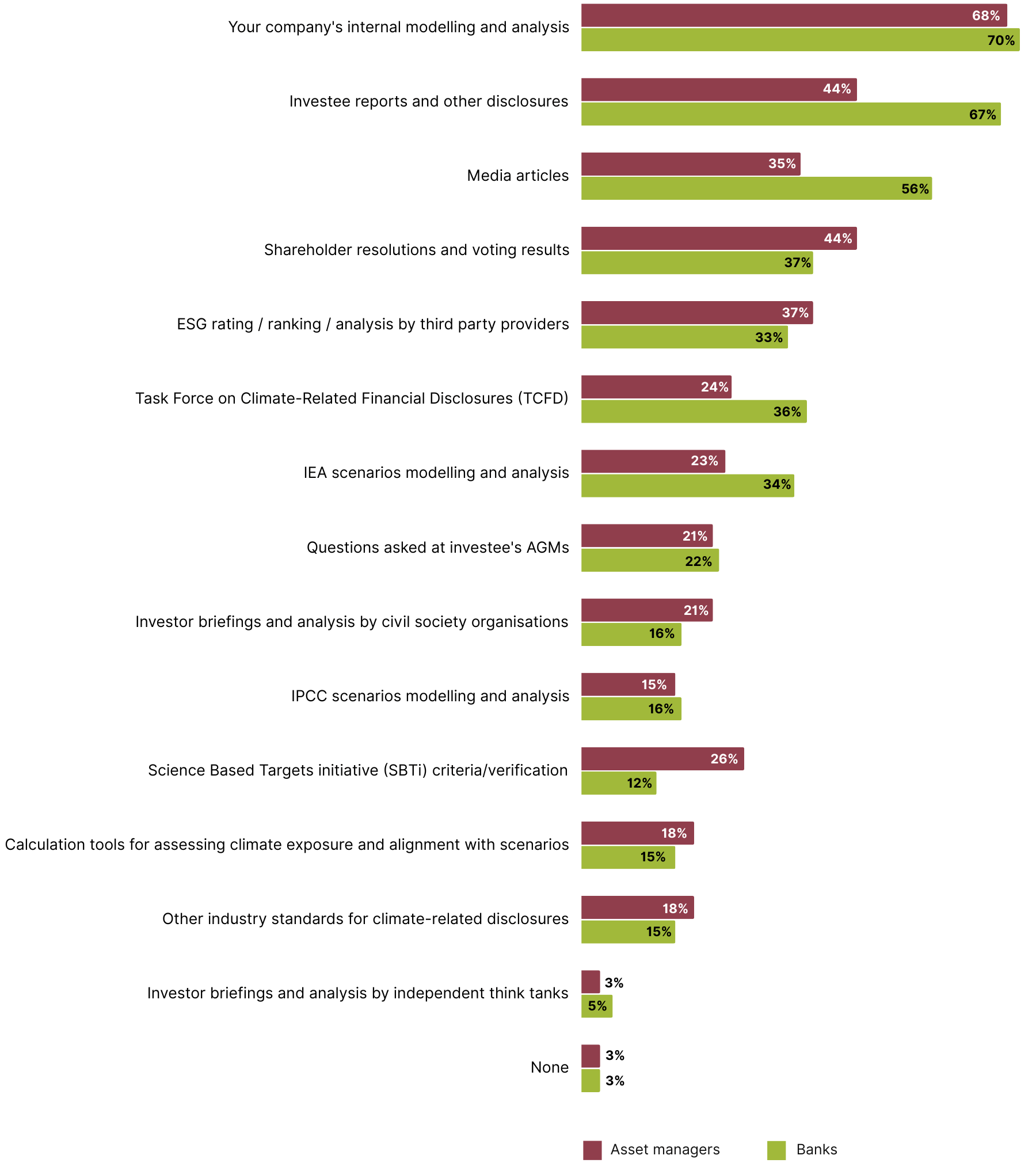

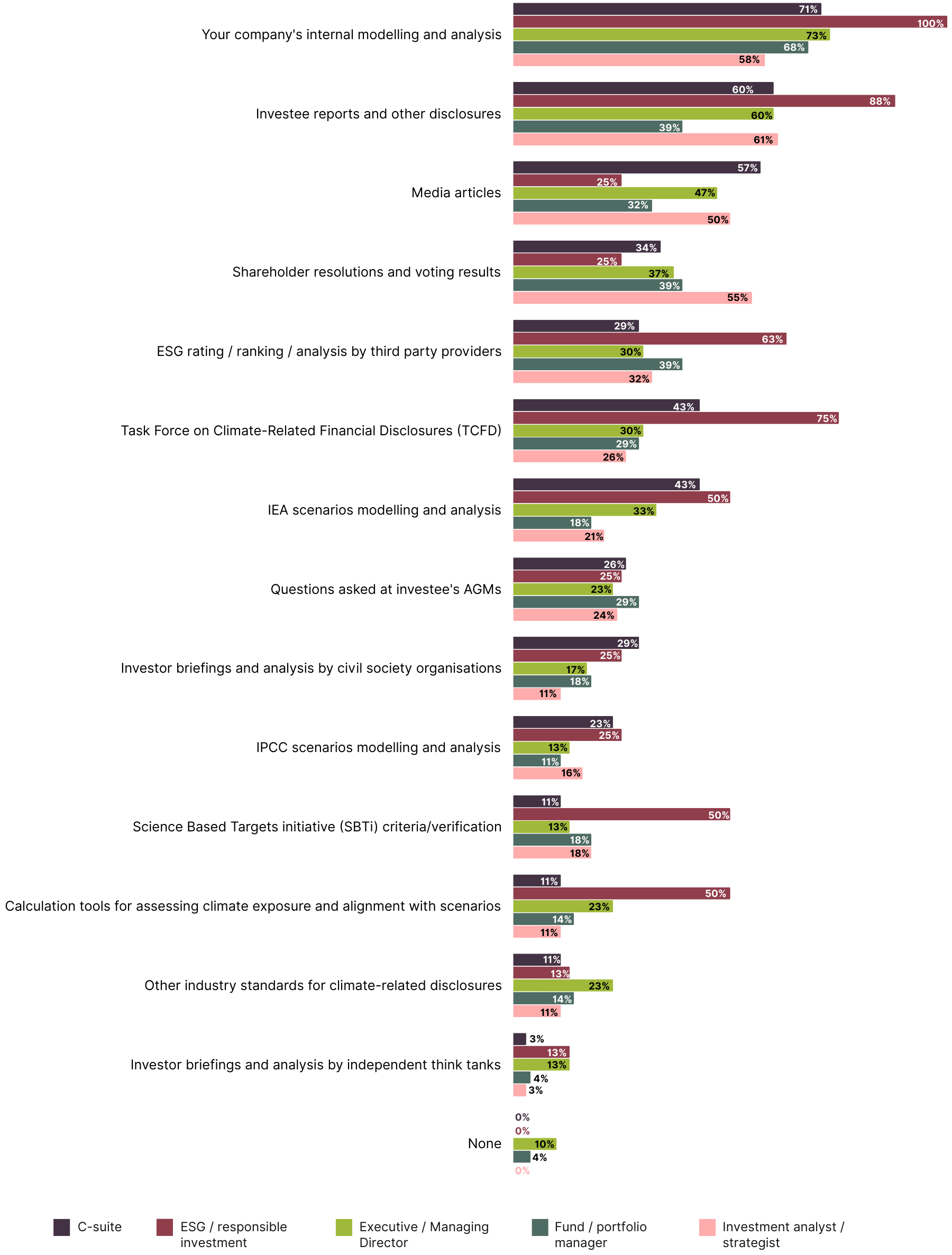

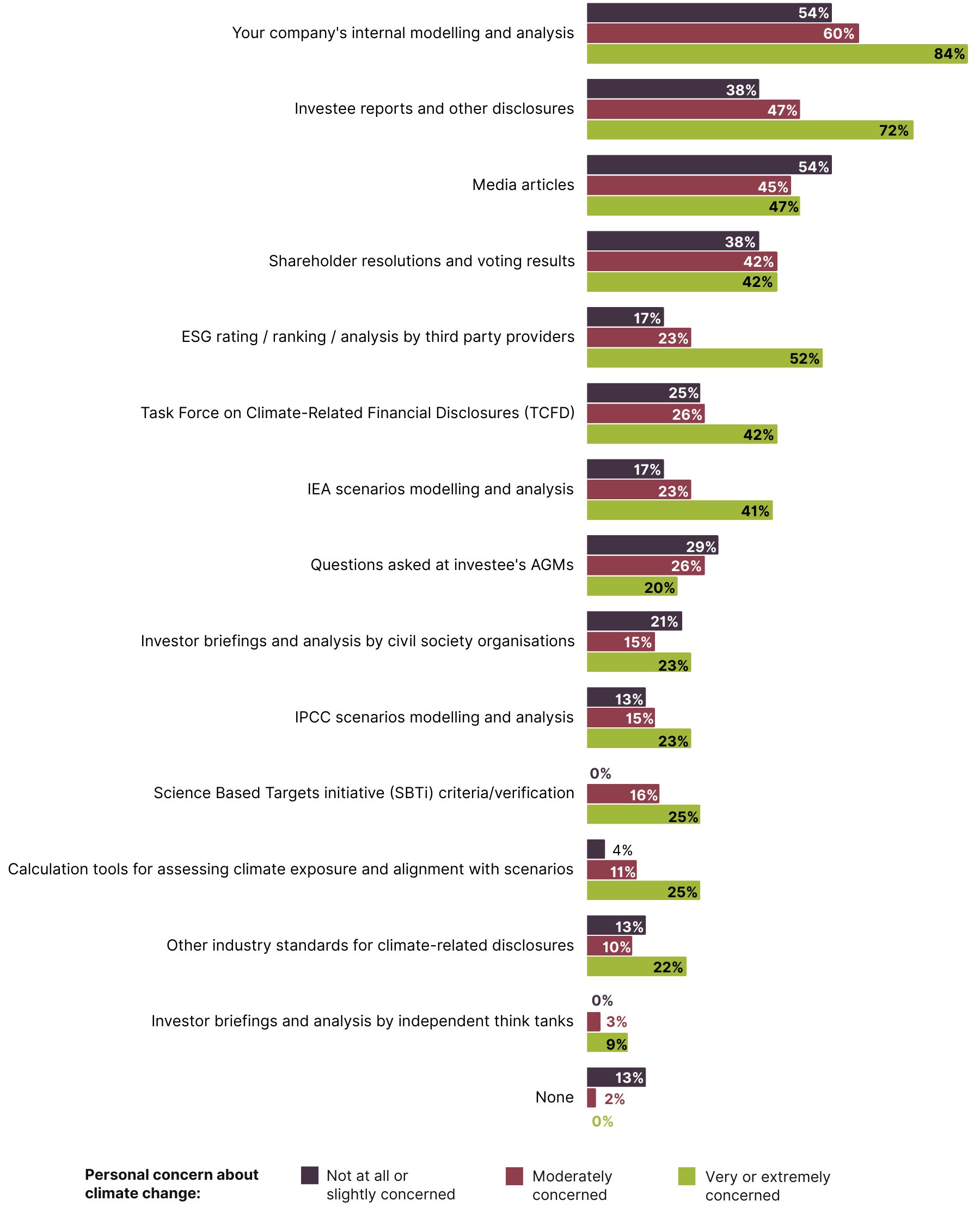

5. Investors are overwhelmingly relying on internal modelling/analysis and investee disclosures when assessing climate risk.

Figure 10: Resources currently used by investors to assess climate risks and opportunities

By region

By company type

By job role

Note: Results for ESG / responsible investment should be treated with caution due to a small sample size.

By climate concern

Quantitative, issue specific, sector analysis from NGOs is most influential especially with regards to energy transition and climate policy/regulation risk assessment, or in areas (biodiversity) where data is generally unavailable

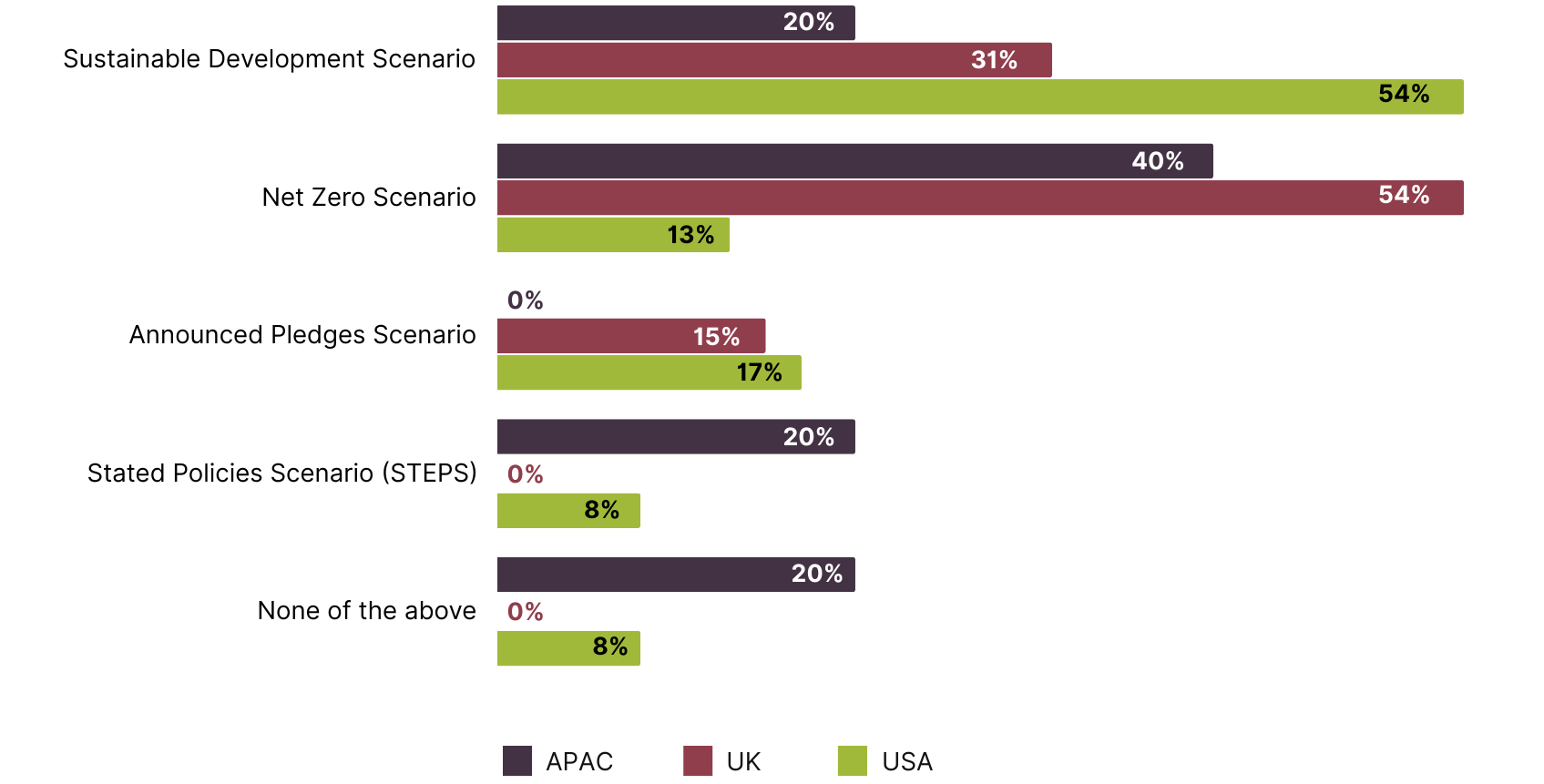

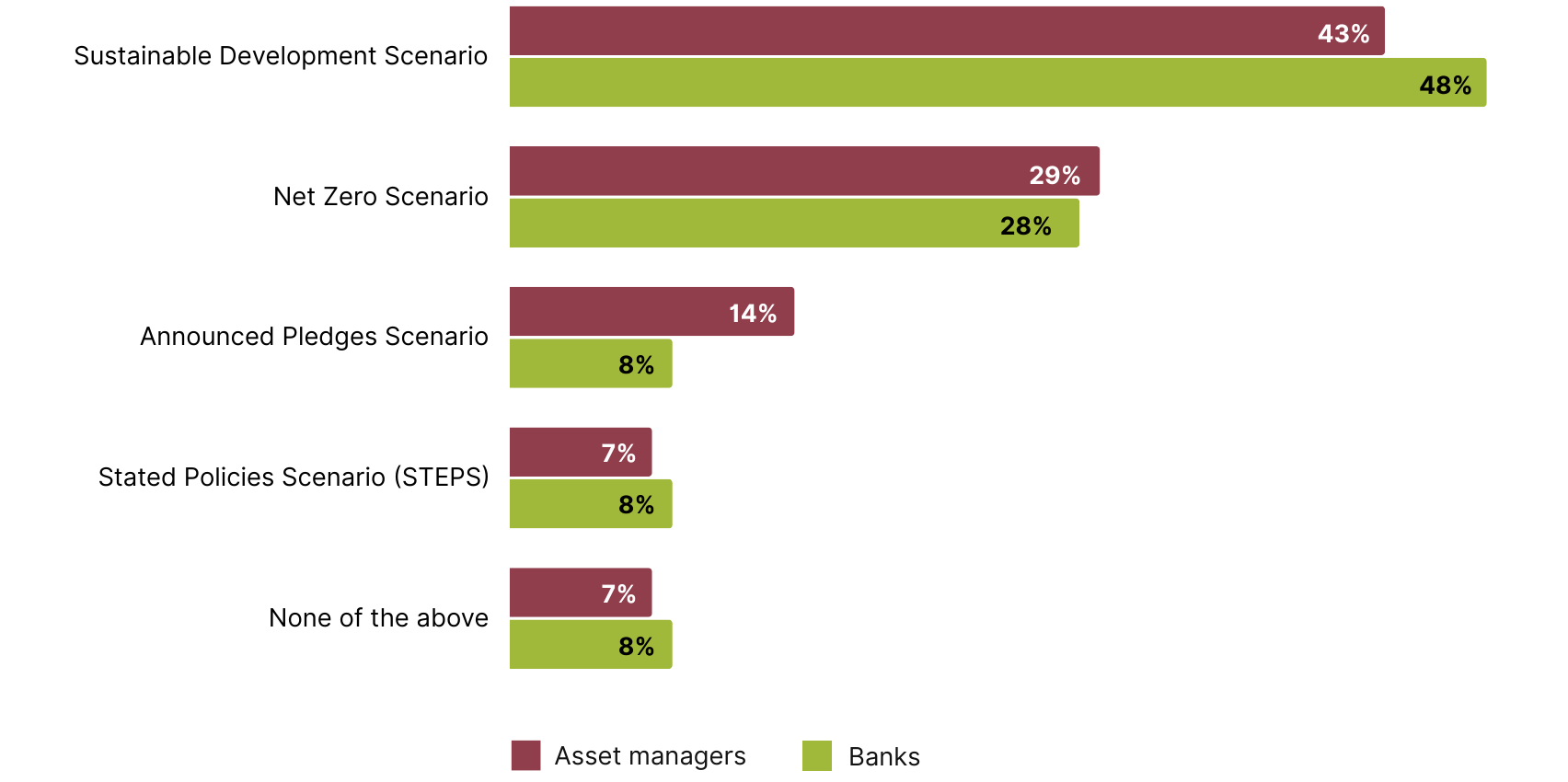

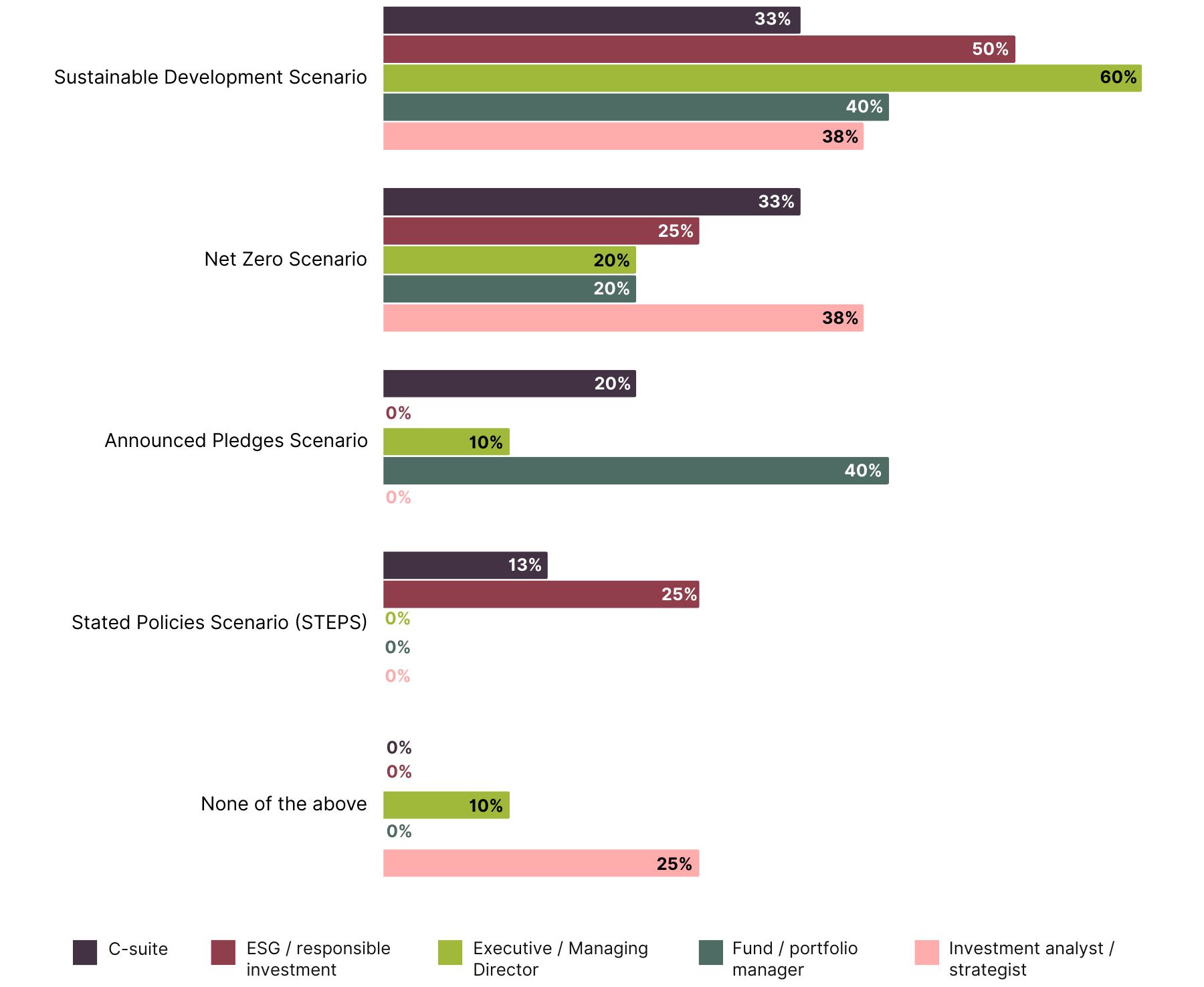

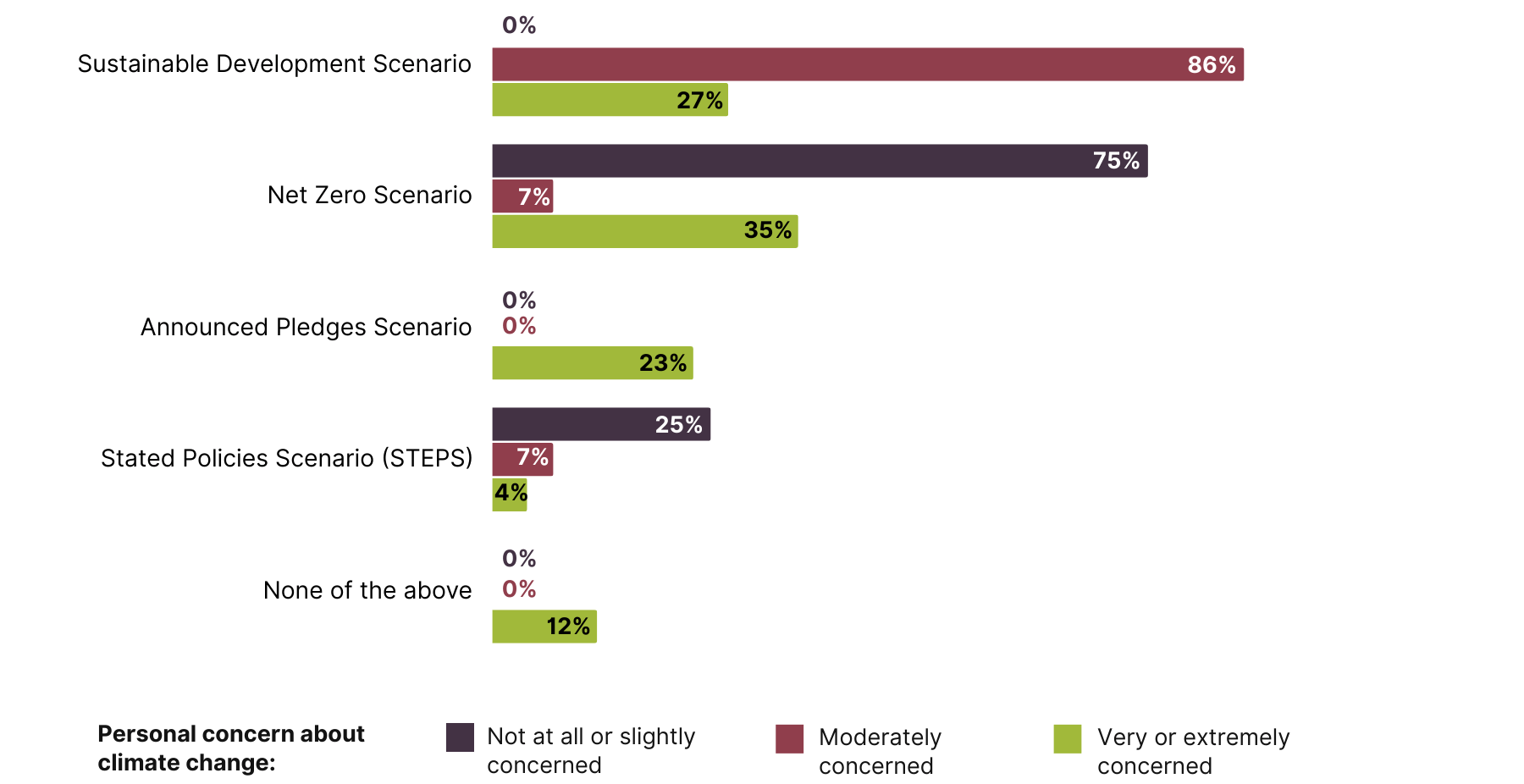

6. Of the IEA’s climate scenarios, investors’ base case modelling is most likely to reflect the Sustainable Development Scenario

Almost one third of respondents indicated they use IEA scenario modelling and analysis when assessing climate risks and opportunities (Figure 9). Of these, nearly half said they consider the IEA’s Sustainable Development Scenario (SDS) to be most aligned with their own base case forecasts (Figure 11). This shows many investors are already ‘pricing in’ a rapid acceleration of the energy transition. The SDS scenario is consistent with limiting the global temperature rise to 1.65°C by 2100 at a 50% probability. It is “based on a surge of clean energy policies and investment”, whereby “all current net zero pledges are achieved in full and there are extensive efforts to realise near-term energy reductions” (IEA, World Energy Outlook 2021, p. 95).

It should be noted that the IEA has stopped using the Sustainable Development Scenario in its World Energy Outlook analyses. The Announced Pledges Scenario (APS) is now the most similar scenario in terms of its assumptions and outcomes (IEA, World Energy Outlook 2022, p. 107).

Figure 11: The IEA climate scenarios most in line with the base case forecast used by investor companies

Degree figures in parentheses are average global temperature rise by 2100 that could be achieved under the scenario at a 50% probability – IEA, World Energy Outlook 2021. Results are only for the 44 survey respondents who indicated they use IEA scenarios in their investment analysis.

By region

Note: Degree figures in parentheses are average global temperature rise by 2100 that could be achieved under the scenario at a 50% probability – IEA, World Energy Outlook 2021. Results are only for the 44 survey respondents who indicated they use IEA scenarios in their investment analysis. Results for individual groupings should be treated with caution due to their small sample size.

By company type

Note: Degree figures in parentheses are average global temperature rise by 2100 that could be achieved under the scenario at a 50% probability – IEA, World Energy Outlook 2021. Results are only for the 44 survey respondents who indicated they use IEA scenarios in their investment analysis. Results for individual groupings should be treated with caution due to their small sample size.

By company type

Note: Degree figures in parentheses are average global temperature rise by 2100 that could be achieved under the scenario at a 50% probability – IEA, World Energy Outlook 2021. Results are only for the 44 survey respondents who indicated they use IEA scenarios in their investment analysis. Results for individual groupings should be treated with caution due to their small sample size.

By job role

Note: Degree figures in parentheses are average global temperature rise by 2100 that could be achieved under the scenario at a 50% probability – IEA, World Energy Outlook 2021. Results are only for the 44 survey respondents who indicated they use IEA scenarios in their investment analysis. Results for individual groupings should be treated with caution due to their small sample size.

By climate concern

Note: Degree figures in parentheses are average global temperature rise by 2100 that could be achieved under the scenario at a 50% probability – IEA, World Energy Outlook 2021. Results are only for the 44 survey respondents who indicated they use IEA scenarios in their investment analysis. Results for individual groupings should be treated with caution due to their small sample size.

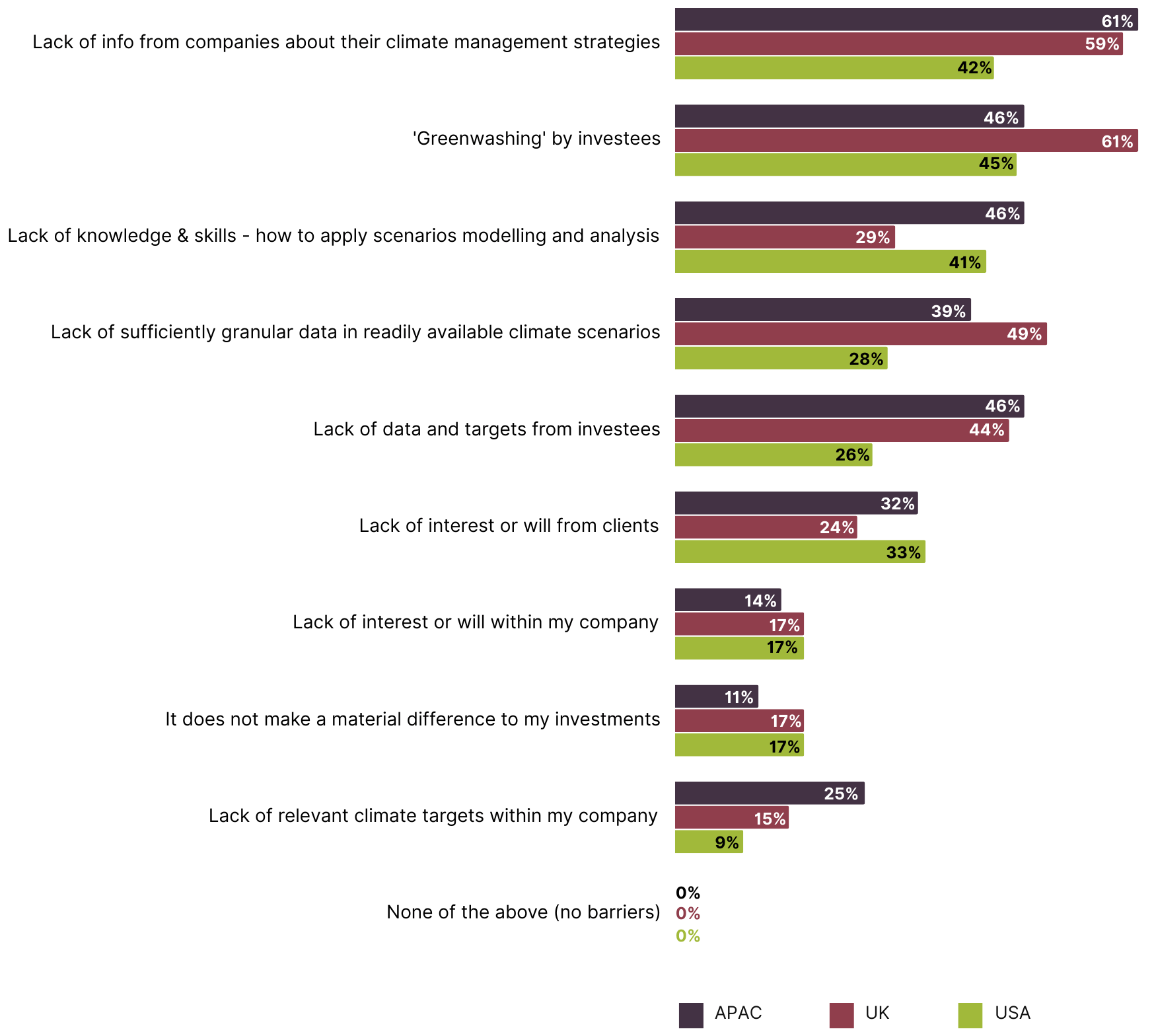

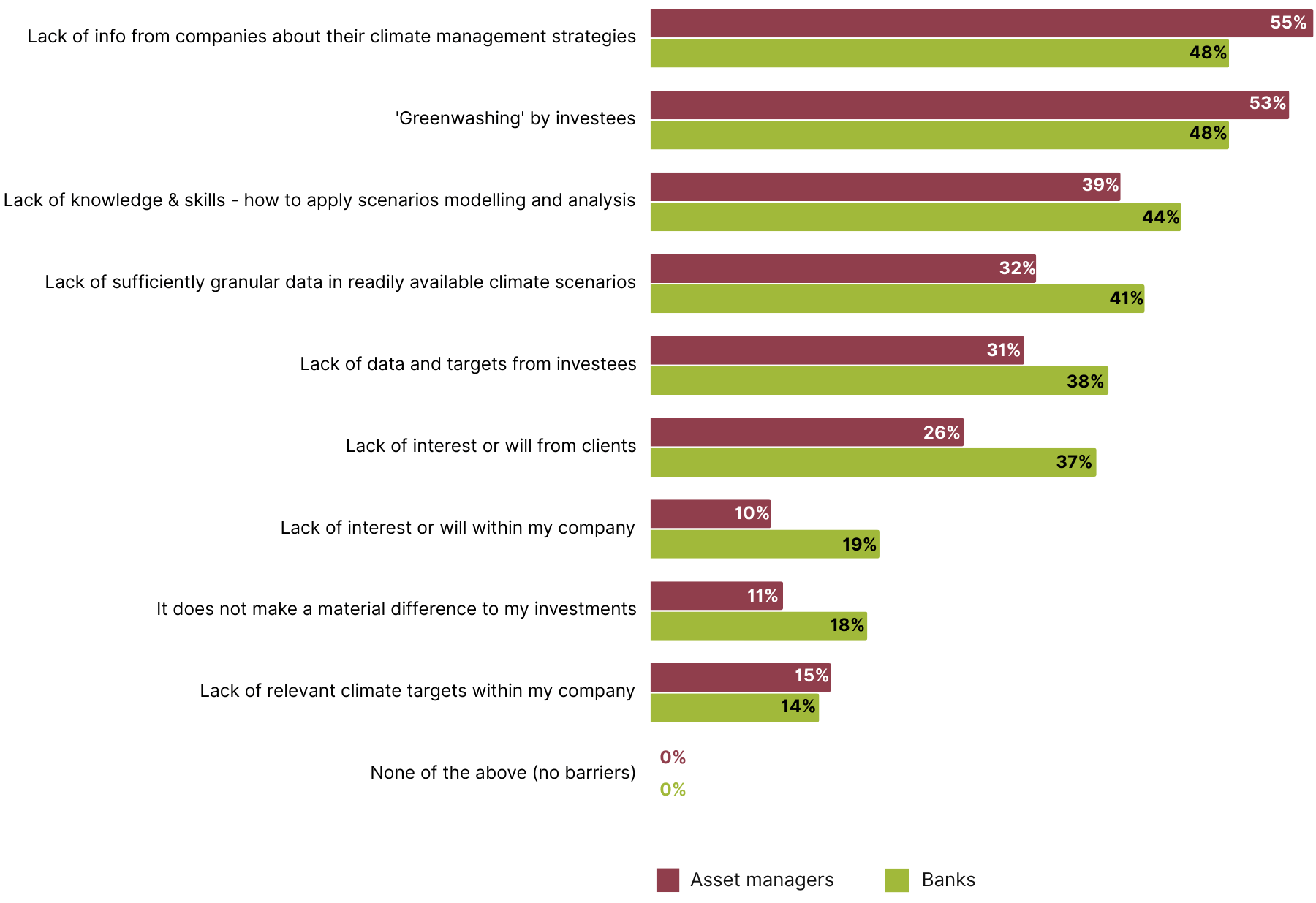

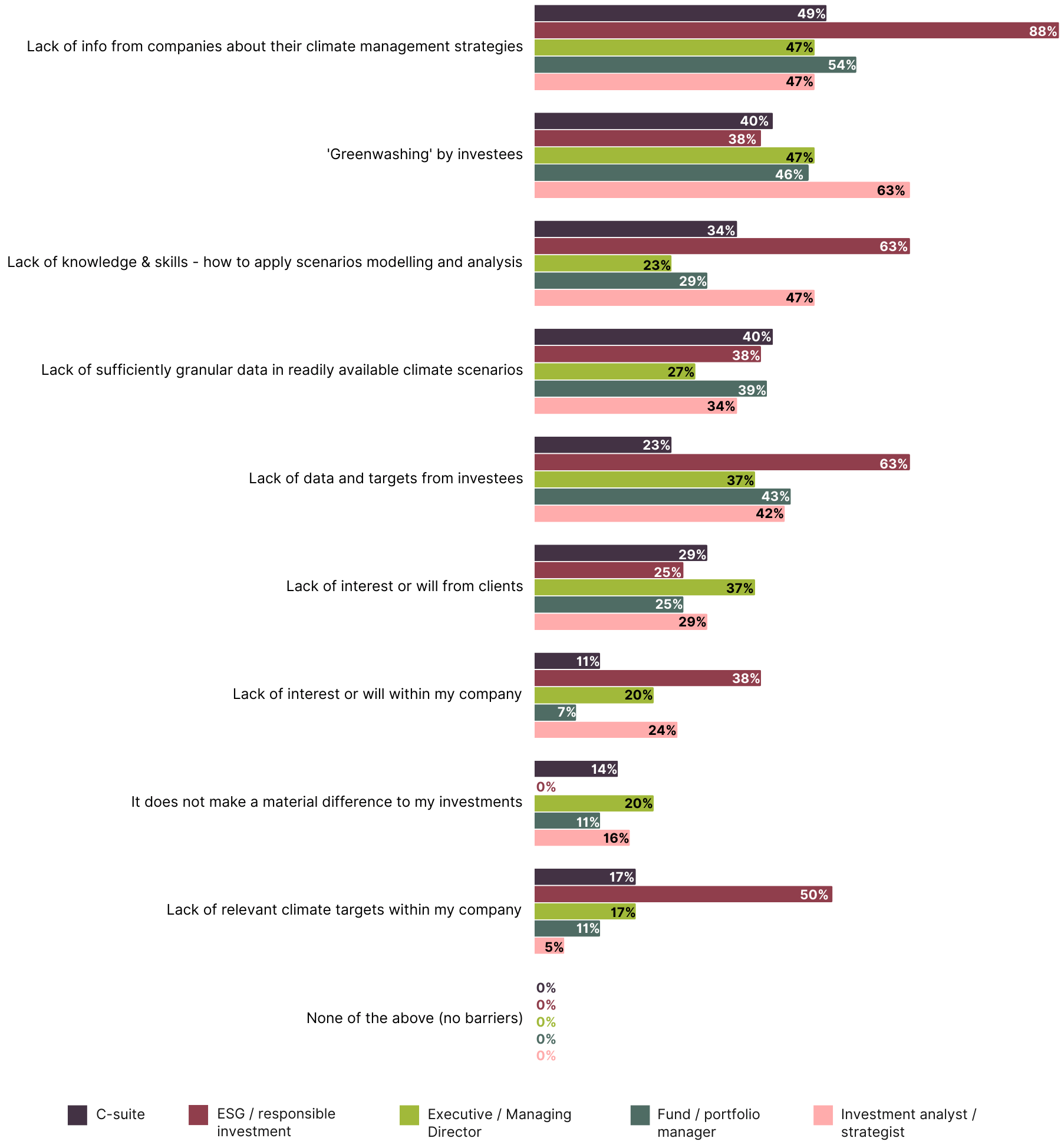

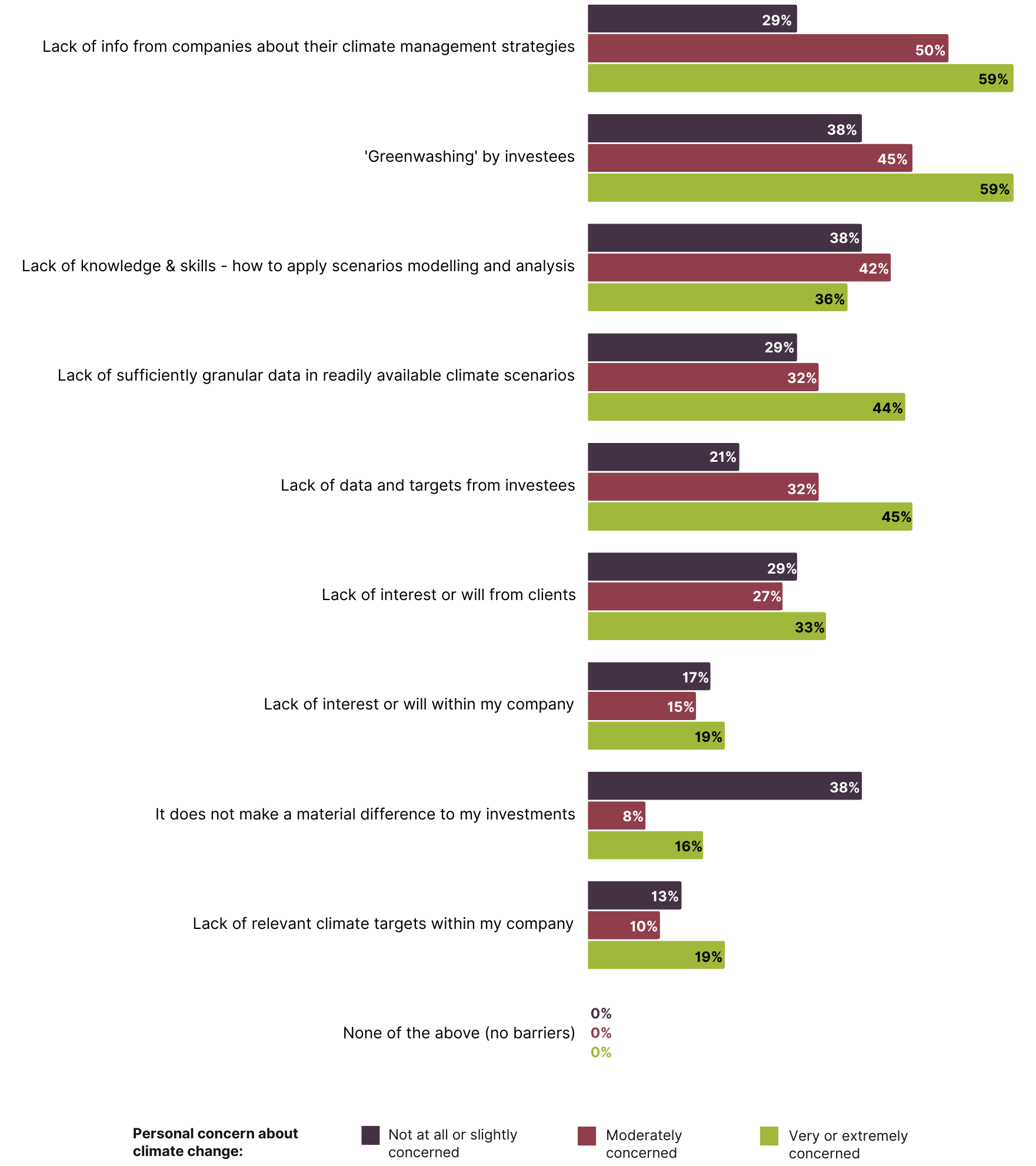

7. Greenwashing and inadequate information from companies on their climate management plans are the main barriers to investors incorporating climate risk more effectively

A lack of knowledge and skills around how to apply climate scenario modelling and analysis, alongside a lack of sufficiently granular data in the scenarios were the next most frequently reported barriers. This is a well-known problem – for instance, the IEA does not include regional pathways in its Net Zero Emissions by 2050 scenario, making it difficult to incorporate into most valuation models.

Figure 12: Key barriers to investors incorporating climate risk assessment into investment decision making

By region

By company type

By job role

Note: Results for ESG / responsible investment should be treated with caution due to a small sample size.

By climate concern

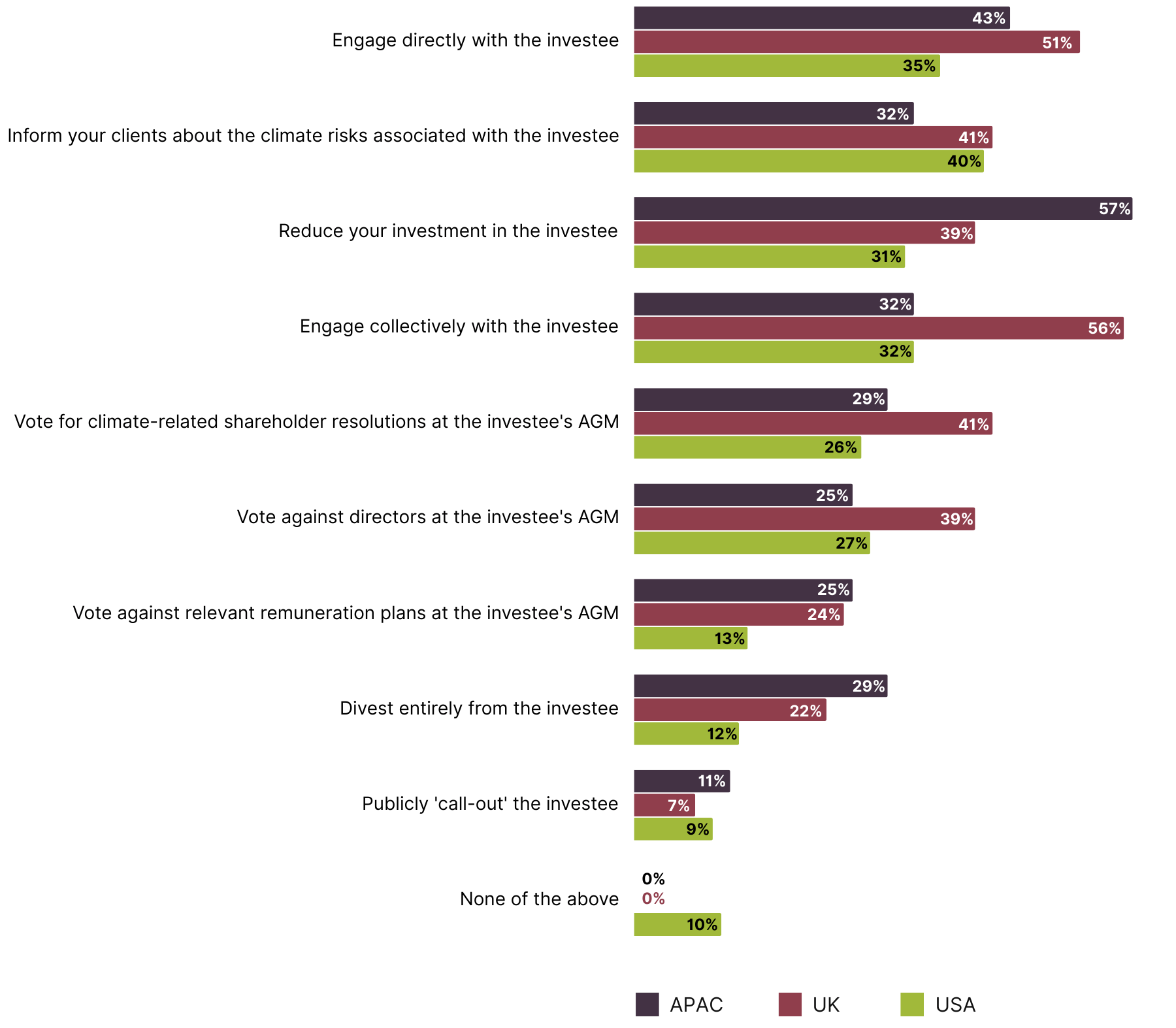

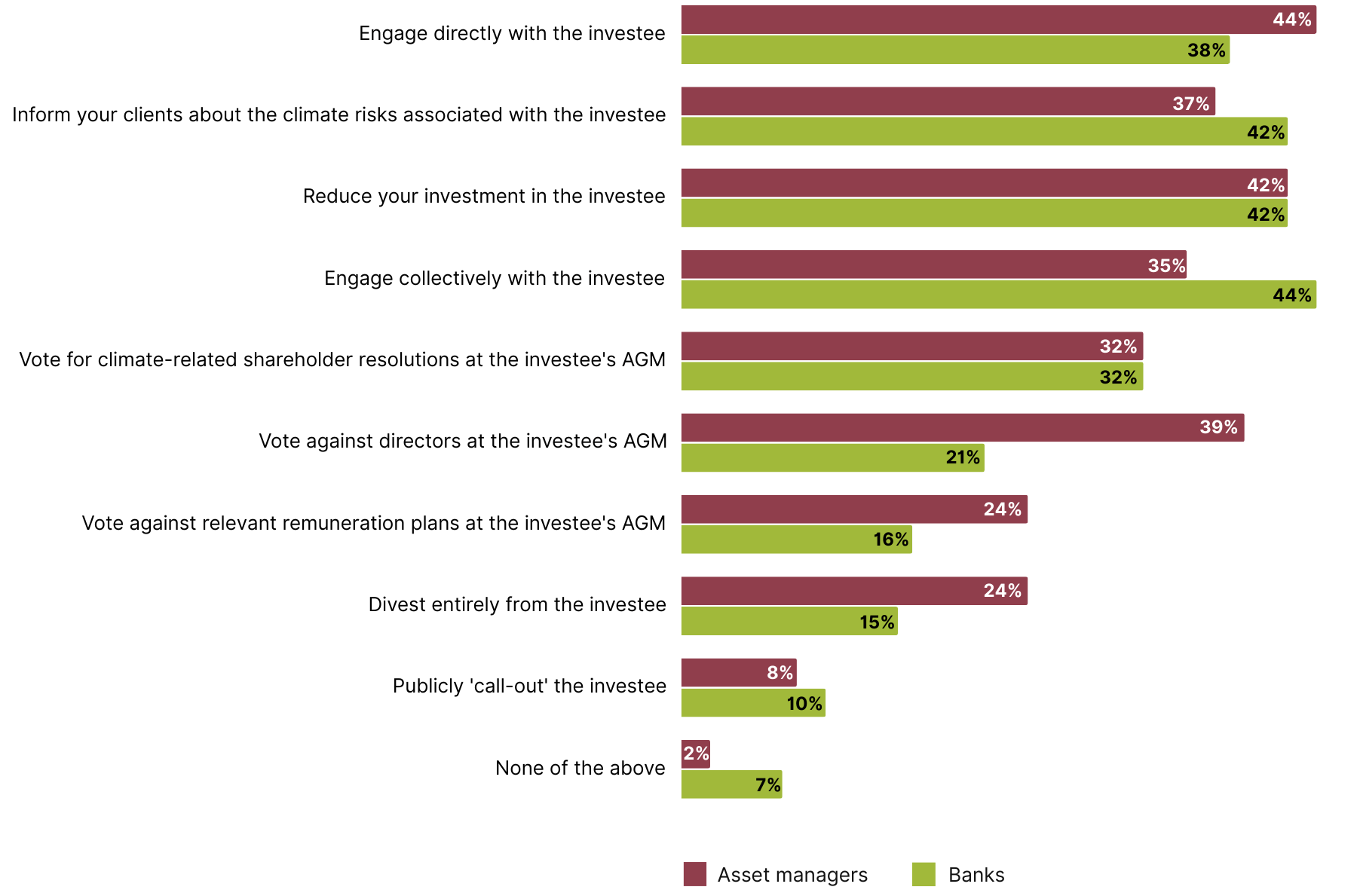

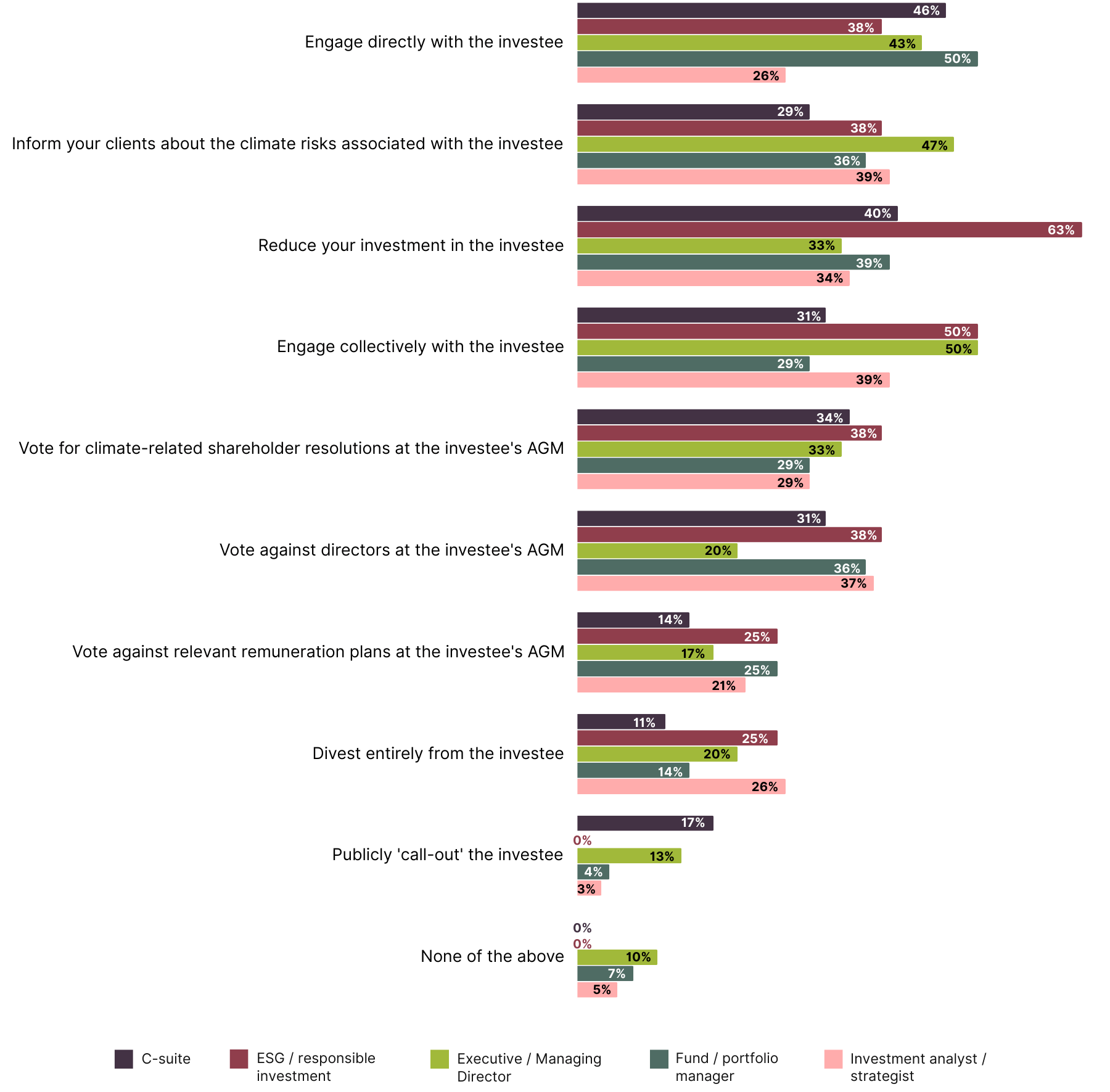

8. Investors are equally as willing to use divestment and engagement with investees in response to climate risks

Figure 13: Actions investors would take if an investee company was found to be facing a high level of climate risk

By region

By company type

By job role

Note: Results for ESG / responsible investment should be treated with caution due to a small sample size.

By climate concern

What would help investors in high-risk companies engage more effectively?

A more prevalent and well informed, granular body of data that is recognised as authoritative, across the investment industry

Climate risk is still not a widely adopted and standardized risk topic. Unfortunately there is a lack of consistent data across market caps and industries. As with any investment, there is a high [degree] of subjectivity, so until that risk can be pretty accurately (and universally agreed upon) quantified it will be difficult to get the industry to agree.

Better and more compelling data and information that climate risk reduction is good for the bottom line.

Other themes included:

“If we had more defined frameworks and regulations it would be easier to hold them accountable because we would know the anticipated action for not managing this risk.” – C-suite respondent, bank, USA

“Clear standards such that greenwashing is called out and frowned upon whereas now the focus is often on virtue signalling” – Investment analyst /strategist, insurance company, Belgium

“Verifiable and standard, transparent assessment and benchmarking tools vs peers, industries and geographic regions” – Executive / Managing Director, asset management, UK

“Reporting and especially standardized measurement and metrics remain an area of significant improvement” – C-suite respondent, bank, UK

Benchmarking (17 comments): More benchmarking data and information (comparing across peers, industry and region), better ESG ratings/scoring.

Better communication and engagement with companies(14 comments): Engaging companies on specific issues, collaborating with companies on target setting, offering support to companies, better access to and engagement with the C-Suite and Board.

Greater transparency / better information from companies (13 comments): Greater transparency in company reporting, greater disclosure from companies on their ESG performance, greater use of independent assessments.

Collective engagement / collaboration (10 comments): Collective engagement with other shareholders, collaboration with other stakeholders to engage companies, supportive networks, utilising regulator shareholders to exert pressure.

Methodology

This research comprised an online survey of 150 institutional investors from more than 100 companies in the USA, UK, Singapore, Japan, Australia, Hong Kong and Belgium. The survey was designed by Market Forces and delivered by market research agency NewtonX during September to November 2023. Rather than using an existing B2B research panel, participants were recruited using NewtonX’s ‘AI-powered’ recruiting process, whereby potential participants were targeted through existing networks, email campaigns, industry groups and digital advertising. A screening questionnaire was used to ensure participants met the needs of the research based on the following criteria:

- Company type

- Location

- Company assets under management (minimum of $20 billion)

- Role within the company

- Level of seniority

- Decision making authority

Soft quotas were applied to the latter three criteria to ensure a good spread of respondents across these groupings. For example, a quota of roughly 25% respondents was applied to the target role groupings (fund/portfolio manager, investment analyst/strategist, c-suite and executive/managing director combined with ESG/other respondents). Previous research on investor engagement with climate risk indicated a bias of survey respondents working in ESG/responsible investment, perhaps due to the nature of the topic and the recruitment methods used. For this reason, we applied an additional limit to respondents working in this field (a maximum of 30 respondents overall), though the survey achieved well under this number (eight respondents).

Respondent profile

Company type

Respondent location

Company assets under management

Role within company

Level of seniority

Decision making authority

1 Krueger et al. 2020; Christophers 2019.

2. See, for example, the Institutional Investors Group on Climate Change’s (IIGCC) Net Zero Stewardship Toolkit, PRI’s A practical guide to active ownership in listed equity, the Paris Aligned Investment Initiative’s Net Zero Investment Framework Implementation Guide, the Investor Agenda’s Investor Climate Action Plans (ICAPs) – Guidance on using the Expectations Ladder and SBTi’s Financial Sector Science-Based Targets Guidance.

Join us

Subscribe for email updates: be part of the movement taking action to protect our climate.