August 2019

Fifty-seven per cent of Vietnam’s planned coal power capacity has faced repeated delay, with postponements to 93% of the projects financed by private, often foreign investors, under the “build-operate-transfer” model. Across the projects, investors are struggling with a cumulative delay of 100 years. Meanwhile, approved solar and wind projects as at July 2019 surpass targets in Vietnam’s power development plan, with the 2025 target for solar PV capacity installed (4 GW) in Vietnam being met six years early.

Vietnam’s Power Development Plan 7, originally published in 2011 and revised in 2016 (PDP 7-revised), plans for 47GW of coal power to come online by 2030. Of this capacity, 3GW was to be abandoned if renewable energy projects proceeded as anticipated.

This planned capacity represents the world’s fourth-largest coal power pipeline, behind China, India and Turkey, according to Global Coal Plant Tracker.

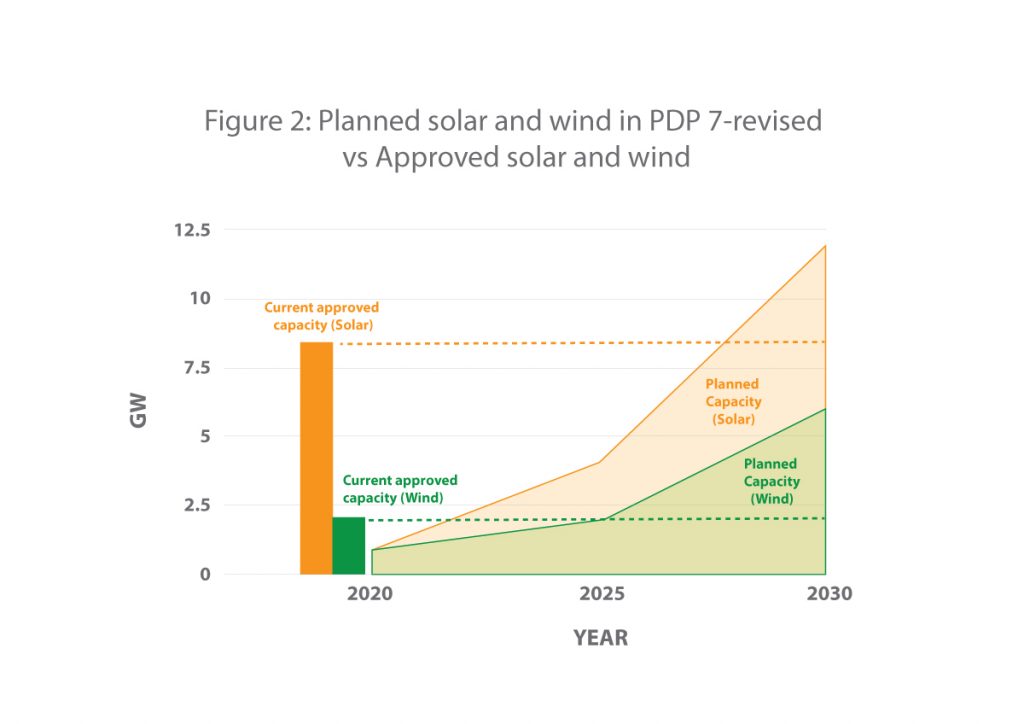

Fast forward to 2019, and the potential for solar and wind energy generation and investor interest have far exceeded the Vietnamese government’s expectations. Currently approved solar PV capacity (8.5 GW) is 10 times the planned capacity for 2020 in the PDP 7 (850MW). Currently approved wind capacity (2 GW) is 2.5 times the planned capacity for 2020 in the PDP 7 (800MW). Some sources suggest approved wind capacity is over five times the planned capacity.

In June 2019, the Ministry of Investment and Trade (MOIT) in Vietnam published a review of the implementation of the PDP 7-revised which shows the planned fleet of coal power will be significantly delayed, with risks for sponsors, insurers and financiers of these coal power stations.

Market Forces’ analysis of the MOIT report (when compared to the PDP 7-revised) shows that:

- 57% of coal power capacity (by MW) in the PDP 7 revised is delayed

- no clear information is available about completion dates for 21% of coal capacity listed in the MOIT report

- 5% of coal capacity in the PDP 7-revised is not discussed in the report

- only 17% of coal power capacity (by MW) is listed as on time

- cumulatively, there is 100 years of delay across planned coal power units.

Of the projects to be financed under the “build-operate-transfer” (BOT) model, 93% are delayed.

Although the rights and obligations of the parties are spelled out in the BOT contract signed with the government, typically it involves private, often foreign companies, designing, building and operating a project for a period specified in the contract, to be transferred to the government at the end. The private company is responsible for raising project finance and retains revenues generated during the period that it operates the project.

Delays to these coal power projects, therefore, mean financial risks to the private companies involved, as discussed below.

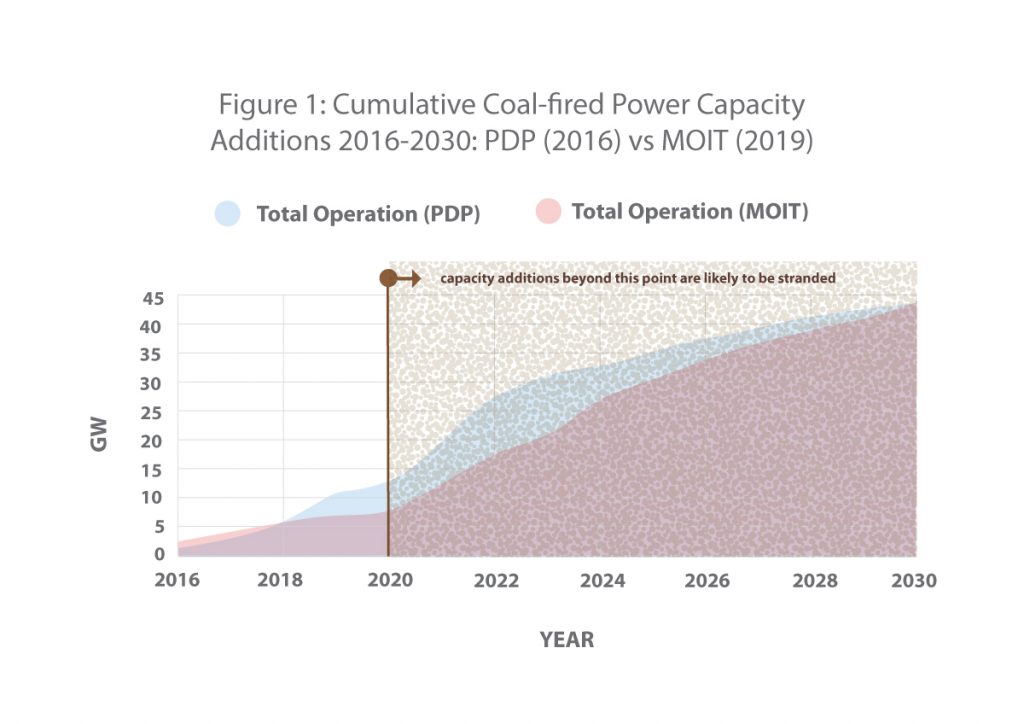

According to the MOIT report, these delays would lead to capacity coming online much later than expected. In the PDP 7-revised, the peak in capacity additions (over 8 GW) was anticipated to be commissioned in 2022. However, that peak is now delayed to 2024 and 2025.

The costs of delay

According to a recent report from financial think tank Carbon Tracker:

- by 2020 it will be cheaper to invest in new solar PV than new coal in Vietnam and by 2021 for new onshore wind.

- it would be cheaper to build new solar PV and onshore wind than to operate existing coal plants as soon as 2022.

This means any new coal capacity commissioned after 2020 (see Figure-1) – an estimated 35.7GW given MOIT’s anticipated delays – could be more expensive to run than renewables and therefore carry significant stranded asset risk. Assuming a capital cost of US$1,400 per kilowatt, this would represent substantial write-offs to coal power investment of approximately US$50 billion.

The causes of delay represent a significant financial risk to the coal project developers, as well as financiers and insurers.

Such delays see money sunk into projects with any hope of revenue being pushed further down the line. Financial institutions are typically unable to sell on the project debt where the project has not started operation and producing revenue. Delays also mean that insurers may have to pay out on claims depending on whether the sponsor has coverage for these issues.

Why have these coal projects been delayed?

A closer look at the delayed projects reveals that various issues have contributed to their postponement, three of which are examined below.

Corruption

Both Long Phu 1 (delayed over 4 years) and Thai Binh 2 (delayed by three years and under risk of further delay) have been embroiled in corruption scandals, with Petrovietnam’s former chairman Dinh La Thang charged for economic mismanagement in January 2018. He was accused of investing approximately $32.5 million of state funds into Ocean Bank against government requirements. In January 2018 he was sentenced to 13 years in jail for diversion and embezzlement of funds and delaying the construction of Thai Binh 2, and 18 years in respect of Long Phu 1.

Trouble with Engineering, Procurement and Construction (EPC) contractors

The financial viability and experience of EPC contractors is essential to a project’s timely completion.

Long Phu 1 has had further delays (see corruption section above) owing to one of its EPC contractors, Russian OJSC Power Machines. This company was added to the US Treasury list of embargoed Russian companies based on Russia’s actions in The Crimea. No major financial institutions can therefore work with the project, leading to no finance provided to the project. Faced with more delays, the sponsor PetroVietnam was tasked with developing a project plan and updating the construction cost. This was estimated in 2013 at US$1.39 billion. As of September 2018, the project was 77 percent complete.

Thai Binh 2’s EPC PetroVietnam Construction JSC has only completed 83 per cent of the project despite working on it for six years. As of March 2019 this project is seeking further financing from sponsor PetroVietnam to push construction forward. The MOIT report suggests that the EPC’s lack of experience has led to these delays.

Nghi Son 2’s South Korean EPC, Doosan Heavy, is also suffering from issues that may lead to challenges for project completion. Despite reaching financial close in April 2018, the project is only 10% complete according to Doosan’s March 2019 audit report. Over the past decade, Doosan Heavy’s share price has fallen from approximately KRW 90,000 to KRW 6,000 in July 2019 and its credit ratings have deteriorated from A+ to BBB (Source: Seoul-based NICE Group). As indicated in Mae-II Economy, over 50% of Doosan’s executives and 7% of its employees have either been downsized or chosen to leave. Many remaining employees have even taken alternating pay cuts.

Local opposition/ problems with resettlement

Long An province, the site of the proposed Long An 1 and 2 coal plants (combined capacity; 2.8GW), has been pushing for the use of natural gas instead of coal in these two projects. While the MOIT does not specify a period of delay for Long An 1, it indicates this project is likely to be delayed and that Long An 2 does not have a specific site selected.

The local residents raised concerns specifically around environmental issues, and that pollution would negatively impact agricultural production and tourism.

Projects like Van Phong 1 have been delayed in part due to lack of consultation about the coal projects, leading to dissatisfaction amongst residents with compensation for land acquisition or replacement of livelihoods lost due to the operation of the plant. Local residents near the Van Phong 1 site have told Vietnamese community organisations that they lack information and are worried about their livelihoods in the resettlement area. The Associated Foreign Press reported how the Vietnamese authorities evicted one such resident, 99-year-old Grandma Ca, and demolished her home to make way for the Van Phong 1. She has refused to leave the site because the new land offered to their family is not suitable for farming. Vietnamese community organisations say that Grandma Ca has now filed a lawsuit in the regional court regarding her forcible relocation.

Solar and wind in Vietnam: Picking up coal’s slack?

The PDP 7-revised was created at a time when expectations for renewables were limited and coal was seen as a low-cost option. The landscape is now very different.

Table 1: Planned renewables capacity (MW, PDP 7-revised [2016])

| 2020 | 2025 | 2030 | |

| Solar PV | 850 | 4,000 | 12,000 |

| Wind | 800 | 2,000 | 6,000 |

In 2017, MOIT’s introduction of a feed-in-tariff (FiT) of US$0.935 per kilowatt hour generated significant interest in solar projects in Vietnam. This scheme was scheduled to expire in June 2019, providing a strong incentive for developers of solar projects to meet this deadline. This incentive has resulted in the 2025 target for solar PV capacity installed (4 GW) in Vietnam being met six years early (See Table 2).

Other sources indicate that solar projects with a total capacity of 12.6 GW are in the pre-investment phase. If these projects proceed to completion, then solar capacity would already surpass the capacity expected in 2030.

Although changes must be made to the grid system to accommodate renewables, a 2018 study by Vietnamese policy NGO GreenID shows it is possible to avoid building 30 GW of new coal power by 2030 by making specific changes to the power development plan, including increasing energy efficiency and increasing renewables to 30% of the energy mix in the new power development plan. A recent scenario analysis by McKinsey & Company found renewables could make up 50% of Vietnam’s power generation mix by 2030, if financial support was provided to improve transmission and battery storage.

The renewables boom and delay in coal power is good news for Vietnam, as it could save the country from building polluting power stations that could easily become stranded assets. The new power development plan is anticipated in 2021, beyond the point when new solar and wind are expected to be more cost effective in Vietnam. This is an opportunity to revise the outlook for where Vietnam’s future power sources will come from, potentially benefiting the Vietnamese economy, the health of its citizens and the global climate.

Companies proposing new power projects will also have cause to ponder their strategies. Coal power has already proven to be a costly option through delays and the social and environmental risks inherent to the technology. The potential to build renewable energy is now demonstrated and companies should pivot their strategies to these clean forms of power that can be rolled out quickly.

Vietnam can make the decision to avoid the risks to financial security, health and environment from coal power and develop safely using renewable energy. For their part, coal developers and financial institutions must stop supporting coal power, build and finance more renewables and help Vietnam make this safe climate future a reality.